PROJECT -2

COMMUNITY WELFARE PROGRAM FUELED BY BLOCKCHAIN AND CRYPTO – PART 1

What does a real and sustainable solution to the wealth gap look like? This Community Welfare Program initiative gives you that insight. It is a strategy to bring this bankless society into the banking system. It is a response to the endless politically influenced debates about a Universal Basic Income. Blockchain and crypto help with that. You will find this and much more in this article.

Author: YS Koen, Klaten, 23 August 2021

Table of Contents

Project -2, Community Welfare Program

FUELED BY BLOCKCHAIN AND CRYPTO

PART 1

What the pandemic has made us all realize is that there had to be a moment of reflection, the realization that we had to get through this together. Schooling, career, relationships, individual growth, everything was put on the back seat for a while, nothing seemed to stay the same and yet there was the feeling of togetherness. Governments came up with all kinds of initiatives to support their citizens, aid programs that provided financial resources to the needy, loan programs for companies were started. Many private initiatives have been launched to help each other, such as a short-term Community Welfare Program. Suddenly, something like a Universal Basic Income seemed necessary and not far away.

The discussion about tackling the wealth gap has been going on for some time, but what kinds of initiatives have been developed so far that actually offers long-term solutions? We believe that no one will morally object to solutions that address the wealth gap. The question is how to achieve these solutions and how can we prevent that what seems like a wonderful initiative today from being shut down tomorrow because it is not so realistic after all? Our biggest objection to an initiative like a Universal Basic Income is that no one offers a solution for how this should be financed in the long term other than through tax increases. Moving budgets from one Social Security program to another is like robbing Peter to pay Paul, when I do that with my company’s balance sheet I am immediately ordered to stop. That are not long-term solutions, but a way to clean up the balance sheet.

Then there are the objections like how much is enough and what is considered sufficient today, will that still be enough in the future? Besides, we don’t hear anyone talking about keeping these kind of programs away from politics. Normally, history is not kind when it comes to such initiatives. There is a great danger that if we allow political interference with Universal Basic Income, it will be used as a negotiating tool during elections. If for some reason the program cannot continue, what will they do for all beneficiaries of these types of social programs? Are they left to their own devices? Do they have to figure out for themselves how to close that financial gap? That’s like giving a heroin addict free methadone first, only to send them back onto the streets a few years later because the free-dispensing program has ended. But in this case, it is the government itself that is the drug dealer.

It shows a lack of intellectual depth within a society if we cannot come up with a sustainable solution to reduce the wealth gap and then opt for the easiest way out by handing out free money. There may be no conditions attached to providing cash, everyone should be eligible. But what does this mean for the further development of an economy of the country in question? We can guarantee that this can only be sustained if the amounts are adjusted over the years and then it is a perfectly valid question, when will it be enough and how much is really going to be enough?

Let’s be very clear in one thing, we are absolutely not against solutions to close the wealth gap. The problem of the wealth gap should have been addressed much earlier. But these kinds of discussions regularly get bogged down in endless conversations without a solution being proposed. News from all over the world is available to everyone, here in Indonesia we also hear about the discussions going on in countries in North America and Western Europe. Everyone here also wants access to the stimulus checks, social security should be a fundamental right for all citizens of the world, but unfortunately that is not the case. Should we leave the discussion to the leading politicians, or should initiatives come from within the society? These are the problems that give us sleepless nights. The pandemic has put the issue of the wealth gap back on top of the agenda. So now it’s time to do something about it. We offer a solution for this. Something that we want to implement here from the beginning and can be expanded around the world in the future. Hopefully, other initiatives will benefit from the road we are paving and the data we will collect will contribute to the adoption of those initiatives.

The Proposal

Providing a credit reserve to members in a group context. Each individual member of the group receives his personal credit reserve. A member can be an individual or a composition of persons such as a family. The group can consist of members of a specific community such as a neighborhood, district, village or a target group that one wants to reach with this program. In the structure in which we want to roll out the plan, the members will be all families within a particular neighborhood community. The credit reserve will consist of 2 x the average annual income per family of that community. The amount is the same for all members, this is not adjusted to each individual member. Each group is united in a “community bank” [1]. The individual members do not receive the money in cash but will be made available as a credit reserve.

We propose that each group has its own foundation/association of which each individual member becomes the beneficiary. The funds ultimately belong to the individual member, the foundation/ association carries out the fiduciary management of the funds. We choose to bring all individual beneficiaries of this program together in a foundation/association because of the group dynamics that can arise. This kind of program, if done right, can help not only an individual member, but also lift the entire community they are a part of to a higher level. In order to get the maximum benefit from the program, information, education and guidance will have to be provided to individual members.

Each member, in our case a family, is allocated a fixed amount. This amount is made available as a credit reserve. It can act as a sort of overdraft facility, where money from the individual reserve can be withdrawn and repaid by the specific members. If members decide to use the amount in full and not repay the debt, the membership will be terminated immediately, and they will lose access to the program. In addition, they will no longer be eligible for support and will lose all other benefits of the program.

In the community that we are going to serve with this project, the project is going to make a very big difference. Especially for the members whose annual income is below the community average. By participating in this program, the beneficiary will build a credit history. Every transaction is recorded from the moment of participation, this can be used in the future when the beneficiary applies for a loan with financial institution. “Giving the unbanked in this society access to the banking system”. Hopefully, this program will also serve as a financial safety net for the beneficiaries. Due to the very limited financial options available to the beneficiary, there is a greater chance that an imbalance will arise when an unexpected event occurs. It is easy to judge that they must learn to save money, but from what? This program provides a financial buffer to fall back on. This may have a positive effect on the mental awareness of the members.

We propose a credit reserve system in which the participant does not have to pay interest on the loan from their own reserve. But there should be a reward and penalty system. Members will be rewarded when they repay on time and will receive a penalty if the money is paid back late or not at all. The latter also applies if participants withdraw more from their individual reserves within the foreseeable future than is justified for the longer term. In addition, it will also be necessary to encourage members to help each other when they need more money than what is available in their own reserve. The community could decide to lend available money to the local business community, of course for a predetermined cost reimbursement and with the borrower providing shares in the company to the joint members. After the loan and the fee due have been paid, a divestment can take place, provided that part of the shares in the company will remain at the disposal of the joint members to be able to opt for future dividend income.

[1] Community banking is a non-traditional form of moneylending. The funds that community banks lend to borrowers are gathered by the local community itself. This tends to mean that the individuals in a neighborhood or group have more control over who is receiving the capital and how that capital is being spent.

What is a Credit Reserve and why do we choose this model?

We have chosen to give the program the term Credit Reserve. Although it’s not an official legal term, or a well-known microeconomic term, we think it covers it all. Let us explain: Each individual member gets their own personal vault (to use another popular word) with a certain amount of money in it, or in other terms a financial reserve. The amount is not provided for consumption, members will derive the most from the program if the principal remains intact, so to achieve this purpose it is provided in the form of credit. Members can withdraw money from their Personal Vault if necessary but are expected to return it when they are able to. It is not a gift, seen from the right perspective it is a financial safety net for unusual events.

Members can withdraw up to a third of the money from their own reserve, but this must be accompanied by an instalment schedule to maintain the benefits of the social program. Up to 5% of the principal can be withdrawn each year without affecting participation in the social program, but we will continue to motivate members to maintain and increase the amount through savings and investments. At least one third of the principal can be used for savings and investments and up to one third of the principal can be used for lending to third parties. Why do we apply so many rules and restrictions? Shouldn’t the program just be unconditional, and shouldn’t we give members unlimited access to the money they’re allotted? Important questions that require a clear answer. But one can assume that we thought this through carefully and thoroughly before coming to this conclusion.

The main reason why we have opted for rules and restrictions on the use of the funds lies in the long-term use of the social program. We don’t want the program to end after a few years and for the members to have had a nice moment at most, but after that everything stays the same. That would be an unnecessary waste of time, burning large sums of capital, but in the end the members are left empty-handed. We do not impose any restrictions on who is eligible for the social program within a particular cohort. In fact, once we recognize a particular group as a beneficiary, each member is allocated their personal money, we will not ask in advance whether or not they want to use the social program, we do not make an exception for an individual member of that community. We believe there are certain benefits to designating a neighborhood community that can participate in the social program and then giving each family of that neighborhood community access to their personal vault, regardless of each family’s personal situation, whether they need it or not. We even assume that up to 10% of a target group independently has a higher annual income than the average of the group. The average annual income of the target group is the most important component for the composition of the amount allocated per member. Members with a higher-than-average annual income are less likely to use the social program to borrow. But that can actually have a positive effect on the group process, because they can use their personal vault to help others in the community when needed. So, no rules and restrictions on the allocation of participation in the program within a certain target group, but certainly rules and restrictions on the use of the principal amount in their Personal Vault by the individual members.

Universal Basic Income vs. Cash Transfers to Personal Credit Reserve

The question remains how did we arrive at the Personal Credit Reserve model? The Universal Basic Income has been discussed several times in this document. The rationale behind the why of a universal basic income is absolutely good, once again the global pandemic has proven this. But if you’re on a continent other than Europe or North America, you will wonder why they have the luxury of having this discussion at all. One of the compilers of this document was born in Europe, worked in his young adult years (total 16 years) on all continents and is now based in Asia since 2008 and mainly in South East Asia since 2012. In other words, two feet in both worlds. Then you start to think that it is precisely here that the need for something like a Universal Basic Income is strongly present. This raises the question of how such a thing should be financed? Tax hike for the rich among us – a drop in the ocean that barely adds anything to make it possible. Increase VAT? In other words, you’re asking the public to pay more for everything in order to enjoy a universal basic income. Maybe we don’t quite get it, but in our opinion that is just pumping money around to keep the machine running and thereby please the public with a universal basic income and at the same time stir public anger by raising VAT.

It becomes even more dangerous if its financing is not properly substantiated, citing as a good example the “Ontario Basic Income Pilot Project”, which was initiated for a period of 3 years. To stop it after 10 months because they thought it was too expensive after a political change of the guard. If these kinds of initiatives are not properly initiated, but you put them in the hands of the government, there is a very great threat that the projects will become the plaything of politics. That may be good for the popularity of the politician at the time, but very threatening for the beneficiaries of the projects. You cannot say that the project in Ontario was not well thought out, see: “Finding a Better Way: A Basic Income Pilot Project for Ontario”, A discussion paper by Hugh D. Segal[2]. But financially not well substantiated to withstand any political wind. It should be noted that it was a pilot project, so it was also something that could be dropped if it wasn’t quite convenient[3]. To keep it under the attention of everything and everyone and maintain the popularity of the initiators, all kinds of catchy names are used and molded into other forms such as social dividend, commonwealth dividend, who doesn’t want such and wants to object to that?[4]

Better documented, better studied and also well thought out are the cash transfer projects in Africa, Kenya and Uganda to be precise. Very well documented projects over a period of many years with clear conclusions. Although they were both projects with a limited duration of one-off up to 3 years, the effects of the programs have been measured and documented over a period of up to 10 years. The conclusions do not differ much from each other, if there are differences in the outcome of the projects, it is at the micro level and certainly not in macro factors. The link to the reports follows at the bottom of the page[5] – [6], but the bottom line, and that is the humble opinion of the author of this paper, is this: The projects immediately made a big difference for the target groups that were allowed to participate in the project, compared to the groups that were surveyed but were not given access to the cash transfers. It provided the beneficiaries with a significant short-term benefit. The benefits even extended beyond the project’s direct beneficiaries, as they actually spent the money.

Over the life of the programs, there is a clearly measurable benefit to the beneficiaries compared to their peer group that does not have the cash transfers. But that benefit immediately diminishes when the project ends, although they still retain some benefit for a period of time built up over the life of the project. Any benefit has completely disappeared within a maximum period of 4 years after the end of the project. Then any advantage is completely wiped out and they are back on par with the others. However, there are many lessons we can draw from the available study material. The most important lesson we can learn from the cash transfer projects is that we need to maintain the social programs for as long as possible to get the maximum benefit for the beneficiaries. Objectives and regulations contribute to clarity about how the resources are spent, a significant part of the resources is well spent when this is reflected in the objectives, at least 70% of the principal is then actually spent on the relevant objective. In this way, dilution of funds can be avoided.

Another clear lesson to be learned from the available reports is that the projects also had measurable benefits for the entire community. The benefit was not only in financial terms, but the projects certainly had measurable positive social impacts. All this has led to how we have designed the social program. We give the participants access to a certain amount as a reserve, part of it can be used to temporarily extend disposable income, but it is not an increase of it, because they are responsible for replenishing the reserve with the same amount they had withdrawn from the reserve. In short, a credit reserve. In addition, a significant portion can be used for savings and investments, allowing them to significantly expand their financial wealth for the future, which they would not have had access to otherwise. This means that they will have less worries about the future and will not have to put pressure on others to make a financial contribution for them, which is common now.

[2] https://files.ontario.ca/discussionpaper_nov3_english_final.pdf A discussion paper written by Hugh D. Segal in 2016, which preceded the pilot project and on which Ontario’s Basic Income Pilot Project was based.

[3] https://maytree.com/wp-content/uploads/Lessons-from-Ontario%E2%80%99s-Basic-Income-Pilot.pdf A report by Michael Mendelson, published in 2019, on lessons learned from the Basic Income Pilot Project in Ontario.

[4] https://assets.website-files.com/5f07c00c5fce40c46b92df3d/5fcf8ed17fb77568bd94cfcb_Potential%20Impacts%20and%20Reach%20of%20Basic%20Income%20Programs%2020201203%20FINAL.PDF.pdf A recent research paper “Potential Economic Impacts and Reach of Basic Income Programs in Canada” published by The Canadian Center for Economic Analysis (CANCEA) in December 2020.

[5] http://cega.berkeley.edu/assets/cega_events/53/WGAPE_Sp2013_Blattman.pdf “The economic and social returns to cash transfers: Evidence from a Ugandan aid program” A research paper by Christopher Blattman et al., published in April 2013

[6] https://econweb.ucsd.edu/~pniehaus/papers/cash_transfers_ge.pdf “General equilibrium effects of cash transfers: experimental evidence from Kenya” A research paper by Dennis Egger, Johannes Haushofer, Edward Miguel, Paul Niehaus, Michael Walker, published on December 22, 2020

A credit reserve, without interest payments, how is that even possible?

The members are each allocated a Personal Vault containing a certain amount of money. If the member in question needs a loan, this is done by means of a withdrawal from the Personal Vault. So, to whom should interest be paid, to the Personal Vault? This complicates the transaction and has a longer repayment period than is strictly necessary to ultimately becoming the beneficiary of the interest payment. There is no reason why we should charge members with interest payments if it serves no other purpose than to complicate the transaction. This also applies in the event that members provide a certain amount of money to other group members in the form of a loan.

In this context, borrowing means that the property of one party is transferred to the other party, who can use it temporarily. This does not mean that the title of ownership is transferred, the right of temporary use is granted to the borrower, but there is a time limit on which the amount must be returned to the owner, which can be in the form of the whole amount, or through installments in a predetermined amount and schedule. All costs associated with the transaction will be nil in the beginning, there will be little to no reason to transfer physical assets other than currency. The transaction may be entirely cash as it is a community transaction and involves relatively small amounts of money. Any costs associated with the transaction shall be borne by the borrower.

But as for business loans to third parties, are those non-interest-bearing loans too? The most direct answer to this question is yes, especially when it comes to members’ ability to provide funds to third parties of a business nature. Interest income is not the only revenue model for providing funds and, above all, not the ultimate solution. If a progressive interest rate is applied, there is clearly a ceiling on earnings. Now others will mainly say that it also serves as security, or to cover risks, but is that really the case? The risk is 100% if the borrower cannot repay the principal. Aside from the risk and limited revenue model, interest hides a very cheap message devoid of any intellectual wealth. A message that strongly contradict the ideas of the social program. Interest has selfish characteristics, when entering into the agreement between lender and borrower, only the interests of the lender are considered. Interest is devoid of confidence in the borrower’s ability to deliver a good result. Interest does not take into account the situation of the other, the borrower repays a certain amount according to the agreement of time and amount, whatever comes his way, if the borrower cannot meet his obligations, he is immediately in default, regardless the reason.

There are other options for establishing a revenue model for providing funds to third parties. The ideas of the social program are more in line with the characteristics of Islamic banking and finance. Below we will list its main features and more specific a particular part of it.

Brief overview of Islamic finance

The contemporary movement of Islamic banking and finance prohibits a variety of activities:

- Paying or charging interest. “All forms of interest are riba[7] and hence prohibited”. Islamic rules on transactions (known as Fiqh al-Muamalat) have been created to prevent use of interest.

- Investing in businesses involved in activities that are forbidden (haram). These include things such as selling alcohol or pork or producing media such as gossip columns or pornography.

- Charging extra for late payment. This applies to Murabaha[8] or other fixed payment financing transactions, although some authors believe late fees may be charged if they are donated to charity, or if the buyer has “deliberately refused” to make a payment.

- Maisir. This is usually translated as “gambling” but used to mean “speculation” in Islamic finance. Involvement in contracts where the ownership of a good depends on the occurrence of a predetermined, uncertain event in the future is maisir and forbidden in Islamic finance.

- Gharar. Gharar is usually translated as “uncertainty” or “ambiguity”. Bans on both maisir and gharar tend to rule out derivatives, options and futures. Islamic finance supporters (such as Mervyn K. Lewis and Latifa M. Algaoud) believe these involve excessive risk and may foster uncertainty and fraudulent behaviour such as are found in derivative instruments used by conventional banking.

- Engaging in transactions lacking “material finality”. All transactions must be “directly linked to a real underlying economic transaction”, which excludes “options and most other derivatives”.

Money on the most common type of Islamic financing — debt-based contracts — “must be made from a tangible asset that one owns and thus has the right to sell — and in financial transactions it demands that risk be shared.” Money cannot be made from money. Another statement of the Islamic banking theory of finance is: “Money has no intrinsic utility; it is only a medium of exchange.” Other restrictions include:

- Risk sharing. Symmetrical risk and return on distribution to participants so that no one benefits disproportionately from the transaction.

Profit and Loss Sharing (also called PLS or “participatory” banking) is a method of finance used by Islamic financial Institutions to comply with the prohibition on interest on loans. Many sources state there are two varieties of Profit and Loss Sharing used by Islamic Finance Intermediaries – Mudarabah (“trustee finance” or passive partnership contract) and Musharakah (equity participation contract). Other sources include Sukuk (also called “Islamic bonds”) and direct equity investment (such as purchase of common shares of stock) as types of PLS.

The profits and losses shared in PLS are those of a business enterprise or person which/who has obtained capital from the Financial Institutions (the terms “debt”, “borrow”, “loan” and “lender” are not used). As financing is repaid, the provider of capital collects some agreed upon percentage of the profits (or deducts if there are losses) along with the principal of the financing. Unlike a conventional bank, there is no fixed rate of interest collected along with the principal of the loan. Also, unlike conventional banking, the PLS Institution acts as a capital partner (in the mudarabah form of PLS), serving as an intermediary between the depositor on one side and the entrepreneur/borrower on the other. The intention is to promote “the concept of participation in a transaction backed by real assets, utilizing the funds at risk on a profit-and-loss-sharing basis”.

Profit-and-loss-sharing is one of “two basic categories” of Islamic financing, the other being “debt-based contracts” (or “debt-like instruments”) such as murabaha, istisna’a, salam and leasing, which involve the “purchase and hire of goods or assets and services on a fixed-return basis”.

One of the pioneers of Islamic banking, Mohammad Najatuallah Siddiqui, suggested a two-tier model as the basis of a riba-free banking, with mudarabah being the primary mode, supplemented by a number of fixed-return models – mark-up (Murabaha), leasing (ijara), cash advances for the purchase of agricultural produce (salam) and cash advances for the manufacture of assets (istisna’a), etc. In practice, the fixed-return models – in particular Murabaha model – have become the favorite model to use, as long-term financing with profit-and-loss-sharing mechanisms has turned out to be more risky and costly than the long term or medium-term lending of the conventional banks.

Mudarabah

Mudarabah or “Sharing the profit and loss with venture capital”, is a partnership or trust financing contract (similar to western equivalent of General and Limited Partnership) where one partner (rabb-ul-mal or “silent partner”/financier), gives money to another (mudarib or “working partner”) for investing in a commercial enterprise. The rabb-ul-mal party provides 100 percent of the capital and the mudarib party provides its specialized knowledge to invest the capital and manage the investment project. Profits generated are shared between the parties according to a pre-agreed ratio. If there is a loss, rabb-ul-mal will lose his capital, and the mudarib party will lose the time and effort invested in the project.

Musharakah

Musharakah is a joint enterprise in which all the partners share the profit or loss of the joint venture. The two (or more) parties that contribute capital to a business divide the net profit and loss on a pro rata basis. Musharakah is often used in investment projects, letters of credit, and the purchase or real estate or property. In the case of real estate or property, the bank assesses an imputed rent and will share it as agreed in advance. All providers of capital are entitled to participate in management, but not necessarily required to do so. The profit is distributed among the partners in pre-agreed ratios, while the loss is borne by each partner strictly in proportion to respective capital contributions. This concept is distinct from fixed income investing (i.e. issuance of loans).

We are not becoming an Islamic financial institution; the social program is an institution for everyone. The key features of Islamic finance are what appeals to us to let our members use them. No hidden costs, no dominant division of roles between parties, clear agreements in advance, no hidden agendas. The social program will not only serve parties with an Islamic background. You can eat the food prepared according to the Kashrut dietary laws without being a member of the Jewish faith, you don’t have to be vegan to not eat meat and you don’t have to be a diehard fan to listen to a song by a certain musician.

The 2007-08 crisis caused a lot of public anger, changes had to be made. All things that made us think and put us on the path of learning, research and development. People like to present things as if they were final, cast in concrete, as if they were statues, but everything is subject to development. The banking system, fiat system, capitalist system and its excesses, but also the reactions to them, it all comes together for us in this project. Things are not as black and white as is often described, something isn’t just right or wrong, that’s not how the world works. First of all, we are all human, almost 8 billion together, we have to keep it all together. Humanity has been on this planet for a while, let’s make sure it stays that way for a long time to come.

That’s why we like to think in concepts, we want to see the important things as a concept, which we can give a twist to so that we all feel comfortable as individuals. We don’t have to blindly accept everything that others determine, everyone can give it their own color, taste and sound. That made us investigate what kind of concept we want to present to the members of the social program, and we came to the conclusion that key features of Islamic finance as a concept better fit with the social program. In fact, we think that if the traditional banking world had adopted more features of Islamic finance, the banking and financial crisis of 07-08 would not have happened so dramatically.

More involvement from all parties is needed to close a deal, but what’s wrong if our members have more insight into what they want to invest money in? There is especially more fairness when an agreement is reached, all parties will have to agree on all fronts, including the division of roles and how the outcome will be distributed. The social program stands for Sincerity, Equality and Opportunity through Cooperation. Then we also have to ensure that that message is properly propagated, and we think this is the best way to do it.

[7] Riba (Arabic: ربا ,الربا، الربٰوة ribā or al-ribā, IPA: [ˈrɪbæː]) can be roughly translated as “usury”, or unjust, exploitative gains made in trade or business. There are two principal forms of riba. Most prevalent is the interest or other increase on a loan of cash, which is known as riba an-nasiya. Most Islamic jurists hold there is another type of riba, which is the simultaneous exchange of unequal quantities or qualities of a given commodity. This is known riba al-fadl. More on Riba: https://en.wikipedia.org/wiki/Riba

[8] Murabaha (Arabic: مرابحة, derived from ribh Arabic: ربح, meaning profit) was originally a term of fiqh (Islamic jurisprudence) for a sales contract where the buyer and seller agree on the markup (profit) or “cost-plus” price for the item(s) being sold. In recent decades it has become a term for a very common form of Islamic financing, where the price is marked up in exchange for allowing the buyer to pay overtime. Murabaha financing is similar to a rent-to-own arrangement in the non-Muslim world, with the intermediary (e.g., the lending bank) retaining ownership of the item being sold until the loan is paid in full. More on Murabaha: https://en.wikipedia.org/wiki/Murabaha

Substantiation & Execution

For the long-term success of this project, we must ensure that beneficiaries receive professional information, education, and assistance. It is likely that without this help, a large majority of beneficiaries will want to spend the money immediately. This will at most give a temporary boost to the local economy and commerce, but in the long run it will do nothing about the wealth gap. Then the project completely misses its goal, at most the beneficiaries will experience a feeling of happiness in the short term, but in the long term this has no effect at all. That is why we want to collaborate with local colleges and universities. This collaboration will be 2-fold, an information and guidance program must be developed, in addition we want to collect data through surveys among members to determine the social impact of this program. The data should provide insight into whether the program has an impact on employment and income, health, and mental wellbeing and what this means for its members. Does the project have other positive impacts on the beneficiaries besides the financial aspects? This data is important for the continuation of the project in the long term.

Once members become convinced of the project’s full potential, that these funds can be used for more than just personal purposes, the entire community will benefit it. We hope there will be interaction within the community. For example, during an impactful event for an individual member, such as hospitalization, death, etc. Then the community could collectively help the individual member by providing financial support for a certain period of time. This can be important when a reward and penalty module is applied. Because the individual member may need more money for the impactful event than their usage limit allows, (more on this later). In addition, we hope that a dynamic will arise that gives people the feeling that more is possible to increase their income independently. For example, by starting a (micro) enterprise for themselves, or by supporting other members in expanding their business.

For business use of the funds, we suggest that the borrower submit a business plan detailing what the funds are needed for, the required investment, term, and repayment schedule. A local investment committee (consisting of the members of the local foundation/association) will study the project in more detail, in addition a request for advice will have to be submitted to the head foundation. If both bodies agree, the local branch, possibly with the support of the head foundation, can make the investment.

Personal use of the credit reserve

This is the most important aspect of the program, the credit reserve for personal use. The target group and community that we serve with this project has little financial scope. They often have not more than their monthly income, no savings, no assets. A project like this will bring significant benefits if each member has access to a credit reserve equal to 2 times the average annual income of the members of the community. The project will have to be promoted in such a way that it is a credit reserve and cannot be regarded as a supplement to the wage income. That is why we are introducing an annual usage limit[9] of 5% of the principal. In the most unfavorable conditions, the whole community will consume its personal usage limit, then the project will end within 20 years. This is not conducive to the survival of the whole project and it loses power for the beneficiaries. Members will begin to view the project as a supplement to their annual income, without opting to experience the long-term financial impact of trying to maintain or even increase principal.

Each individual member can withdraw up to one third of the principal from the personal credit reserve if a repayment plan is executed for this. In this way, the member retains all the benefits of the entire program. However, strict adherence to the repayment plan must be ensured otherwise the member will lose access and benefits of the plan. In order to enable a significant withdrawal from the personal reserve, the beneficiary will have to submit an application. It will have to be described what the necessary funds will be spent on, accompanied by a repayment proposal including how many installments and the installment amount. The request to withdraw money from the personal reserve is dealt with in a personal meeting with the beneficiary, possibly with a counter-advice. In that conversation, the beneficiary will be informed about the possible consequences if the repayment plan is not strictly adhered to. The responsibility for withdrawing funds from the personal reserve and complying with the repayment plan rests entirely with the beneficiary and must be respected.

The individual credit reserve can be used in whole or in part to put together a savings and investment portfolio that can increase the principal in the long term. The capital gains accrue directly to the beneficiary and can be spent as the beneficiary chooses. The capital gain can be paid out after a certain period as a supplement to the annual income or can be kept in the savings and investment portfolio to maintain and further expand the capital. There will have to be clear communication with the individual members about the risks associated with any investments. That is why a risk profile will be mandatory, in which certain agreements will be registered. The head foundation is responsible for strict adherence to this protocol.

[9] Annual Usage Limit: Members can withdraw up to 5% of the total amount of the credit reserve annually without refunding this amount and still retain access to the program.

Making funds available to third parties in a personal capacity

Members within a group are expected to support each other where necessary. We recommend that members, for arbitration purposes, notify the local foundation/association in advance should the transaction occur between members. If the members concerned jointly decide not to inform the local foundation/association in advance about the transaction, neither of them can claim support if a dispute arises between the members about the transaction. The foundation does not wish to promote transactions with third parties outside the group and will therefore not be a party to this. Members are strongly advised not to become personally involved in transactions outside of their own group.

We do not prefer transactions by one or more members in a personal capacity with a commercial party (company). Especially because the right of recourse for private individuals is expensive and limited. We advise everyone to make such a transaction through the local foundation/association. In the event of an emergency, several parties jointly bear the burden and not a limited number. On the other hand, if the foundation rejects the transaction, members in a personal capacity in a group context, can still decide to financially assist the commercial party. If one or more members still decide to enter into the transaction with the commercial party after a negative assessment by the foundation, then no claim can be made for assistance from the foundation if things threaten to go wrong.

Making funds available to third parties from a group context

All group members are given the opportunity to apply for a business loan within their own group. All individual members are given the opportunity to invest up to one third of the credit reserve in companies through such credit applications. Each loan application must be accompanied by an investment plan with principal and repayment schedule. The loan application is first processed by the board of the local foundation/association and then submitted to the head foundation for advice.

If both bodies agree with the credit application, it is put to the vote of the members. If the project is accepted by the members after a successful vote with an absolute majority of two thirds (66.7%) of the votes, the project will be accepted for funding by the whole group. A member of the group who has voted negative can request not to participate in the group investment. If the members vote positively with a democratic majority of at least 51% of the votes, only the members who voted positive will participate in the investment. If the funds within the own group are not sufficient, an appeal can be made to the head foundation for additional investment funds. If a funding application is accepted by the group with an absolute majority of votes, the head foundation is obliged to make up any shortfall in funds.

Pledge of the credit reserve

If one of the members needs external financing, the relevant member can submit a request to use the credit reserve as collateral for external financing. If the member concerned has used part of its individual credit reserve for purposes other than the future loan, the outstanding part will have to be repaid, or that amount will be deducted from the collateral on the credit reserve. Double pledging of the same collateral cannot be permitted under any circumstances.

The credit reserve may only be pledged to an official financial institution. The foundation must be informed by the lender about the conditions of the pledge. Exercise of a claim based on a pledge of the credit reserve by third parties may affect further participation in the program for the member concerned. If the claim exceeds one-third of the credit reserve, further participation of the member concerned in this program will have to be reassessed after the claim transaction. If a claim is made due to the member’s breach of contract, participation in this program will be irrevocably terminated. All agreements and provisions for the use of pledge will be documented and processed until the transaction (collateralization) is terminated.

In all cases, individual members can count on support and guidance from the (local) foundation/association. From the beginning of this program, all the procedures of the program will seem complicated to members, so we want to continue to emphasize the importance of information, education and support. The program will lose momentum if members are left to their own devices and there is a good chance that individual members will pursue only short-term happiness without realizing what this program can do for them in the long run. Once the project is fully developed and all possibilities can be exploited, all procedures will be more efficient for the benefit of all members.

Project Infrastructure

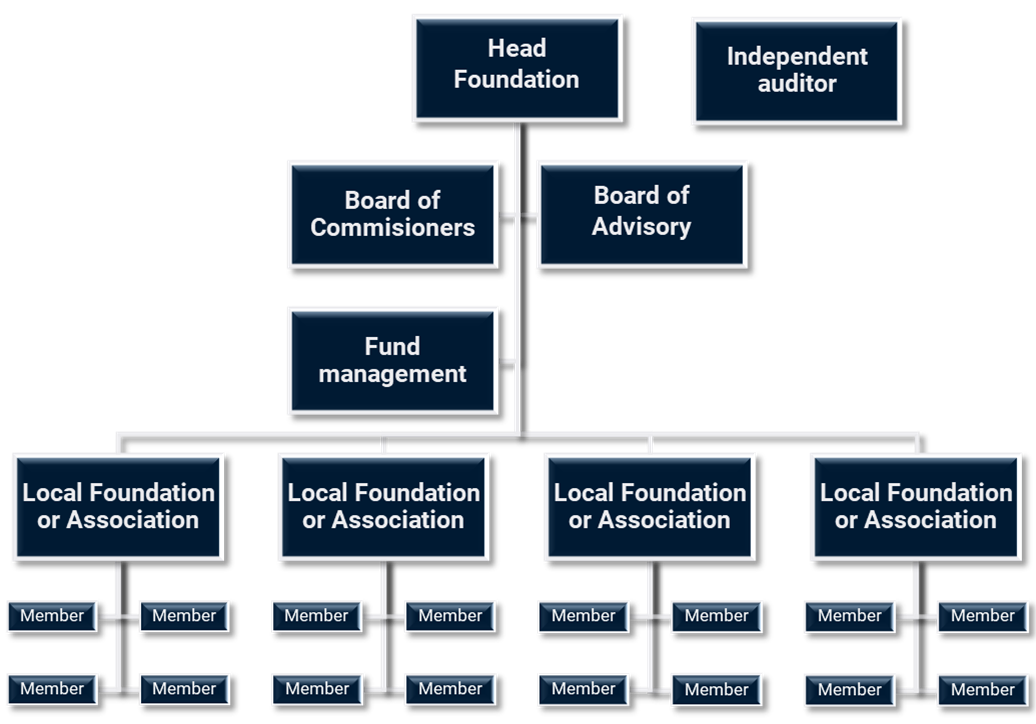

Head Foundation

This foundation will be established in Indonesia, where we will roll out the project. It is therefore logical if the initiators want to establish the foundation there. This foundation will take care of the management and governance of the (local) projects that we have under direct management. The head foundation has no executive tasks in the various “local” projects other than a controlling and supervisory task. The head foundation will have an executive board of at least 2 members, chaired by the chairman, who comes from the initiator P.T. Emas Cemerlang Bersama. The board is supported by a supervisory board and an advisory board. They will be jointly responsible for the general policy of the project and where necessary changes in the policy will be applied to ensure the longevity of the project.

In addition, the head foundation is responsible for managing the funds that have not yet been allocated to the various “local” projects. A manager will be created for the management of the funds, who will explain and implement the policy in this regard. In addition, this manager must ensure that the cash reserve for the various projects is maintained and they will have a monitoring function over the spending of the funds at the local projects.

Local foundation or association

This will be a legal entity that will carry out the operational activities of the project. They will be responsible for allocating and managing the funds to the target group. The local foundation or association will be subordinate to the head foundation and will have to report to the head foundation from its executive role. The local foundation or association does not have a decisive vote in the admission of new candidate members but can at most advise the head foundation.

The local foundation or association must have a physical presence in the community they serve. They must support the beneficiary members of the program. From this position, the local foundation or association will have to carry out activities so that the beneficiaries can use their credit reserve. In addition, the local entity will be responsible for informing, assisting and educating the beneficiaries and has an executive role in the reward and penalty system that the beneficiaries have to deal with.

The local entity must establish a Council of Members representing the group of beneficiaries, these individual council members must attend at least the monthly meeting to report on the implementation of the program. In addition, loan requests from third parties can be discussed and loan requests from individual members that exceed the set limit can be approved or rejected. The board of the local entity chairs the monthly members’ meeting and sets the agenda but leaves room for input from the members’ council. In addition, the board must provide the individual members with a report on the state of affairs of the local entity at least every calendar quarter. This can be done in the form of a newsletter to all members, in which there is also room for information and education.

Board of Commissioners and Advisory Board

The main task of the Board of Commissioners will be to monitor the performance of the social projects. Together with the general board of the foundation, they determine the policy of the project in all facets. In addition, they ensure that the general management fulfills its duties properly. The Board of Commissioners will consist of at least 3 board members from the start of the project. The members must have sufficient experience in general business operations, legal affairs, and fund management. The Board of Commissioners reports directly to the chairman of the foundation, independently of the general management, who in turn also reports to the Board of Commissioners and the chairman. The Board of Commissioners has an official character, and, in its role, it is held responsible for the policy and regulations of the project.

The Advisory Council will be established to advise on matters such as structure, legislation, procedural matters, permits and legal obligations, but will not be limited to advising on the aforementioned matters. The Advisory Board is not affiliated with the general management or the Board of Commissioners. However, both administrative bodies can approach the Advisory Council for advice in all kinds of areas. Both the general management and the Board of Commissioners can nominate candidates who are eligible for a position on the advisory board. Members of the Advisory Board do not have to be elected by vote. However, the entire board, or at least a majority of the board, will have to support the appointment. There is no term attached to participation in the advisory board.

The head foundation, but also the local foundations or associations can make use of both bodies. The Board of Commissioners can mainly be consulted when it comes to the implementation of policies. The advisory board can be consulted when the local entity wants to propose changes in operational policy and activities, however the local entity should not make any changes on its own without clear instructions from the head foundation. The local entities are executive bodies, the main foundation is in charge of the policy and structure of the entire project.

Fund Management

Fund management is entirely separate from the general management of the foundation, it will be a separate department directly under the responsibility of the chairman of the head foundation and the Board of Commissioners. Fund management makes the policy for the funds that have not (yet) been allocated or spent to/by the members. The task of fund management will be to maintain and possibly expand the funds under management so that more members can use the program in the future. A clear policy plan will have to be implemented in which various issues must be explicitly answered. Once the policy plan is approved by the Chairman and the Board of Commissioners, the fund manager is fully responsible for the implementation of the policy. The policy plan should be made public available so that everyone has access to it. Reports must be published quarterly and annually, with the fund manager being accountable for implementation in accordance with the policy plan.

There will have to be a clear policy for 3 phases:

- Short term: up to 1 year, this will mainly be about the liquidity of the funds for direct allocation and use to the individual members.

- Medium term: 1 to 5 years, investment, and spending policy for funds under management and funds allocated to individual members but are left unspent.

- Long term: more than 5 years; The focus for this phase will be mainly on the funds under management of the program which will be allocated to new members in the future, or which will have to ensure the stability of the whole project.

In addition to managing the project’s general funds, the fund manager will also be responsible for developing savings and investment products for individual members. This can be done in-house or outsourced to third parties, as long as the fund manager provides sufficient options. When it comes to product range of third parties, the fund manager is responsible for the risk assessment of these products and the fund manager will have to communicate clearly with the external product manager the risk profile of the individual members.

The fund manager will also have to play an explicit role in providing financing to third-party commercial parties that submit a loan application to the project. The fund manager is responsible for a thorough risk analysis when providing the financing. In addition, if deemed necessary, the fund manager makes an amount available to cover the financing. The fund manager will also serve on the board of directors of the company, which receives the funding, on behalf of the members of the project. This will be a supervisory role and not an executive role as a borrower’s board member.

In the next part of this documentation, the role of the fund manager and the weight involved in carrying out the work will be discussed in more detail. That is also the reason why we believe that the fund manager should not come under the general management of the foundation. The fund manager will have his own executive board that will fall directly under the responsibility of the chairman of the foundation.

Independent auditor

The independent auditor is instructed to review the financial reports of the foundation and the fund manager on a quarterly and annual basis and provide an opinion. Both the general board of the foundation and the board of the fund manager will have to determine independently of each other together with the auditor in which standard format they report. The auditor is expected to process his findings in his report and submit this to the Board of Commissioners and the Chairman of the foundation. A request will also be made to the auditor to publish this report. More on this will become clear in part 2 of this documentation.

Summary & Conclusion Part 1

With this we would like to conclude part 1 of this document. This Social Program is a workable alternative to all the good intentions surrounding the Universal Basic Income. This is not a temporary solution to the wealth gap problem, but a sustainable project that can last a lifetime. The members do not have to worry that the Social Program will stop as soon as the allocated government budgets are empty or if someone else thinks it is too expensive. Each individual member is allocated a budget in a Personal Vault at the start of the program. The members themselves are in control of the budget and determine the spending policy. We hope that with what has been described above we have made clear what our intentions are and how we intend to implement the social program.

“Never let a good crisis go to waste”, the famous words attributed to Winston Churchill, as well as to Rahm Emmanuel, President Obama’s chief of staff at the time, he also came up with similar words: “You never want a serious crisis to be lost,” at the occasion of the banking and financial crisis of 2007-08. If we have learned anything from the crisis, it is that the public has become more aware of what money is and all the excesses that come with it. But otherwise much remained the same, less than 2 years later the major banks acted as if nothing had happened. Governments went into debt to clean up the mess from the banks and it was the public who got presented with the bill and ultimately had to paid for it.

The rich among us have not suffered, the richest person on earth had an estimated net worth of $62 billion in 2008, the richest person on earth has amassed about $175 billion in wealth in 2021. The public doesn’t notice such when they look at their bank account. However, we cannot say that nothing happened at all. Soon after the 2008 crisis, the talks around a Universal Basic Income became louder and louder. In fact, less than 10 years later, America had someone running for office on this subject, Andrew Yang. It is therefore a subject that needs to be looked at seriously, especially its possibilities and impossibilities. Then we automatically come to one of the most difficult issues, how should that be financed? There doesn’t seem to be an appropriate answer to that.

This also translates into all initiatives that have been carried out, if they are not cancelled prematurely, then often it stays silent after the first trial period. The world doesn’t seem to be ready for it. One can point to low interest rates and then suggest that we can borrow cheaply. But that is of course extremely dangerous, because you are walking on slippery slopes when it comes to the longevity of the project. Because what happens if the interest rate rises sharply, or do we hold monetary policy hostage because the interest rate cannot go up, otherwise we have to disappoint many people. Look at Japan and then think again. It should come as no surprise that a reaction from the public was to be expected in this area. The answer came in the form of crypto tokens (Bitcoin etc.) and blockchain technology. This was long dismissed by the establishment as a gambling element and not to be taken seriously, but they also started working with blockchain technology. With a market cap of $2 trillion in 2021, we can no longer speak of something that cannot be taken seriously. It’s still speculative, but what else could we expect?

Then the world plunged into a global pandemic and now no one can deny anymore that something like a universal basic income really needs to be looked at seriously. But if we follow the discussions on this, there is still no suitable answer ready for the financing issue. What we think is even more important is that there should be an initiative from the public, but what is being done so far, it is being debated and beyond that it is only looking at why governments are not doing anything. So, we came up with an initiative ourselves. It is not presented as a gift, because: “There ain’t no such thing as a free lunch”. But with the alternative we came up with, we’ve created something that will last a lifetime. The details can differ for each target group, but the framework is in place and we will share the data in due course in the hope that others will also take up this project for their region.

In part 2 we take a closer look at what drives this project, how it is made financially possible without having to facilitate large amounts of money every year. What is the ecosystem driving this project?

A publication of:

P.T. Emas Cemerlang Bersama

Axa Tower Lt.45, Jalan Prof. Dr. Satrio 18, Karet Kuningan, Setiabudi,

12940, Jakarta Selatan, DKI Jakarta, INDONESIA

Tel: +62-821-1377-8883