PARTICIPATING

IN STARTUP FUNDING

Convertible Note – € 1.000.000,00 – first tranche of € 500.000,00

*** This project document was first published on December 16, 2020. We have revised and rewritten the entire document. The document is now correct for the current situation. This document is part of a series of 3 project documentation. ***

PARTICIPATING IN STARTUP FUNDING

Prologue

Participating in start-up financing is not always possible for everyone. We’ve all heard the stories of people bragging about their exorbitant profits from investing in a Start-up ventures. Who has ever wondered when you will get the chance to participate? Start-up financing is also not for every investor, if you are looking for a quick profit, then you should not invest in a start-up, because the horizon is often shrouded in mist. If you can’t take a risk with the money you invest, you should stay far away from investing in a start-up. But if you are interested in the journey that any start-up investment will take you on, if you want to be involved in any way, then it could be the investment that will give you great satisfaction. Because if one thing is certain about a start-up venture and investment, it will take you on a journey that is sure to collect memories along the way. Still interested in what we have to say, read on.

Author: YS Koen, Klaten, 18 September 2021

This documentation is part of a series of three documents in which we explain the goals we want to achieve. To achieve these goals we need partial funding, as the projects are much larger than what we can accomplish with our own resources. This documentation discusses the structure in which we offer the necessary investment. It concerns the contract form in which we record the agreements between the company and the investor, the form in which we offer the investment and the associated legal certainty. Because if there is one thing that is important about start-up financing, it is the trust that the investors must be offered. Trust/confidence that we will deliver on what we promise to do, that we will do everything we can to make these projects run smoothly and reach the finish line, even if we don’t know exactly when and where that will be, at the beginning of the journey.

The projects that we (will) undertake may be new, but the house (the company) in which this takes place is certainly not newly established. Founded in December 2015 and successfully completed the start-up phase some time ago. We have written extensively about how the first years went and how we experienced this personally[1]. These are the projects that are in the start-up phase. Although that term is also deceptive, because starting up, are we only now starting the projects and is it still questionable whether 1 of the projects will ever be realized? Certainly not, a few years ago, in mid-2018, we encountered a problem that urgently needed to be addressed. It is a problem that we encounter daily in the workplace of one of the operating companies that we manage. It is a problem in an industry where no significant innovation has been made for more than 40 years. That is often fatal for a sector, were it not for the fact that it is a sector that produces goods that belong to the necessities of life and for which we, with almost 8 billion people on this planet, are grateful that production continues (clothing production). Identifying a problem that bothers you so much that you can’t relax until you find a solution to it is always the best breeding ground for innovation.[2]

The second project is of a completely different order[3]. This project will have a very big impact for the beneficiaries. No shortage of potential users. It is a subject that for the first time in recent history came to prominence during the Great Depression of 1929 – to the late 1930s. During every economic crisis, you see the topic reappear at the top of the agenda. Hundreds of books have been published about it, by proponents and opponents, and generations of academics have dealt with this subject. But despite all the good intentions of everything and everyone, there is so far no sustainable solution that survives the critical phase. So why are we so complacent to think we have that solution? Some reasons:

- Initiative from society

- No political interference

- No government influence on implementation

- Satoshi Nakamoto

We continue with the contents of this document.

Convertible Note explained

A convertible note is a financial instrument that contains a written promise from one party (the issuer or creator of the convertible note) to pay another party (the beneficiary of the convertible note) a specified amount, either upon request or on a specified future date. A convertible note usually contains all the terms and conditions related to the debt, such as the principal amount, interest rate, maturity date, date and place of issue, and the signature of the issuer.

Although financial institutions can issue them (see below), convertible notes are debt securities that enable businesses and individuals to obtain funding from a source other than a bank. This source can be a person or a company willing to carry the note (and provide the funding) under the agreed terms.

Executive Summary:

Convertible Notes Are a Hybrid of Debt and Equity

- Convertible notes are originally structured as debt investments but have a provision that allows the principal plus accrued interest to convert into an equity investment at a later date.

- This allows the original investment to get done more quickly with lower legal fees for the company at the time, but ultimately gives the investors the economic exposure of an equity investment.

- Typical terms of convertible notes are interest rate, maturity date, conversion provisions, a conversion discount, and a valuation cap.

The Pros of Convertible Notes

- Convertible note financings are simpler to document from a legal perspective, meaning that they are less expensive and quicker to execute.

- Convertible notes avoid placing a valuation on the startup, which can be useful particularly for seed stage companies which have not had enough operating history to properly set a valuation.

- Convertible notes are good bridge-capital or intra-round financing options.

The Cons of Convertible Notes

- If future equity rounds are not completed, the convertible note will remain debt and thus require redemption, potentially pushing still-fragile companies into bankruptcy.

- To avoid the above, terms and conditions can be set that, if taken too far, defeat the purpose of the convertible note and end up taking as much time and effort as a traditional equity round.

- Certain clauses such as the valuation cap and the conversion discount can complicate future equity raises by anchoring price expectations.

Convertible notes have become increasingly popular in the world of startup financing, particularly in seed stage companies. However, before going down this path, it is important to understand the potential pitfalls of this type of financing and whether or not it is the best choice for your company. We will first give a brief overview of the basic concept of a convertible note and how it has some attributes of both debt and equity, and then we will look at the pros and cons of this form of financing.

The Basics:

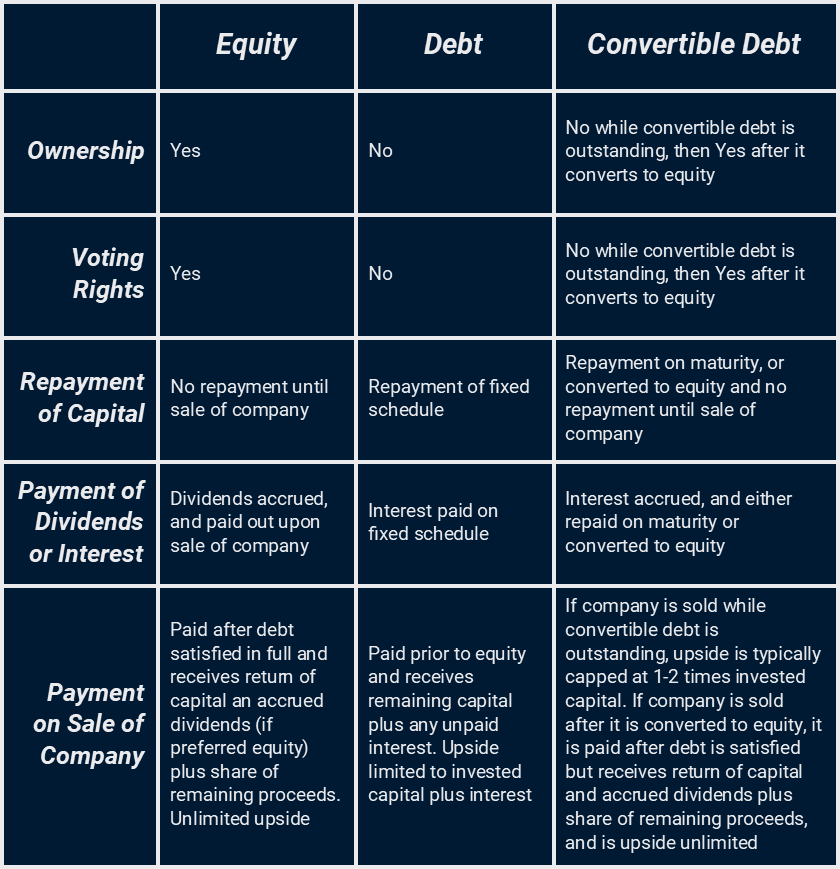

Equity Investments

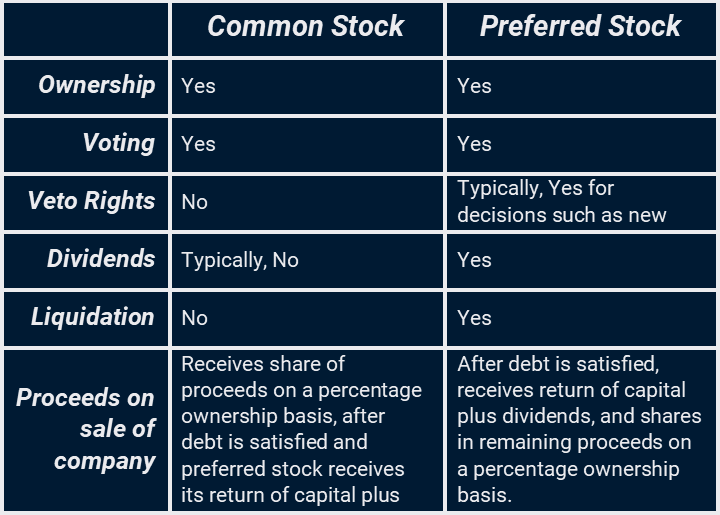

When most people think of an investment, they are thinking about equity. In an equity investment, a company sells a percentage of their company (equity) for a sum of money. When a company raises funding by selling equity, there is no set schedule for the investor to get repaid, and the investor generally counts on making their money back, plus a return, in a future liquidity event (such as an acquisition of IPO) or through distributions of future profits. In a typical venture capital investment, an acquisition or IPO is almost always the way that investors make their money, with distributions of cash flow being a rarity. Another key point about equity investments is that because the investor is a part owner of the company, they typically have some sort of voting rights that govern various decisions of the company.

Most equity investments in venture capital-backed companies are structured as preferred stock, which is different than simply $X for Y% of the company. When the investment is structured as preferred stock, this typically comes with terms such as a liquidation preference, a preferred dividend, and approval rights over certain company decisions. In most types of preferred stock, the liquidation preference means that in a liquidity event, the investors get the value of their investment back, plus any preferred dividends, prior to the rest of the funds being distributed amongst the % ownership. The preferred dividends are generally not paid in cash but accrued and paid out when there is a liquidity event. As common stock is generally owned by founders and employees of the company, this means that all the investors must be paid back plus a guaranteed return (the preferred dividends) prior to any funds being distributed to the common stock. In addition to regular voting rights, the preferred stockholders also often have additional approval rights over items such as the terms of subsequent rounds of financing and acquisition opportunities.

Common vs. Preferred Stock

Debt Investments:

The most typical type of debt is a loan with a set schedule for repayment of principal and interest. Assuming the company can make the payments, the investor knows what return they are getting in advance. Given the uncertainty of early-stage startups, debt is not very typical when it comes to funding this type of risky venture. However, there are some institutional investors that provide debt to later-stage venture-backed companies, particularly those with recurring subscription payments such as SaaS companies.

There are a few notable facts when it comes to debt. In contrast to equity owners, debt holders do not have an ownership interest in the company and do not have voting rights. However, when it comes to the priority of payments in a liquidation scenario, debt holders are paid in full before equity holders, so it is perceived as a less risky investment. When it comes to the complexity of documentation and legal work that goes into setting up various investments, it is simpler and less expensive (at least in reference to a typical startup funding deal) to structure a debt deal in comparison to equity.

EXAMPLE: An investor purchases €25.000 of convertible notes that carry an 8% interest rate and a 20% conversion discount. In a qualified financing that occurs 18 months after the convertible notes are sold, the company sells equity at €3,50 per share. At this point, the notes will have accrued €3.000 in interest, making the amount owed to the note investor €28.000. With the 20% discount, the conversion price for the notes is €2,80 per share, and the investor receives 10.000 shares of the new stock. Had the investor waited to purchase the stock at the time of the qualified financing, they would have received 7.143 shares of stock, so it is clear there is a big reward to the convertible note investor for taking the risk of investing earlier.

Convertible Notes: A Hybrid of Debt and Equity

In short, convertible notes are originally structured as debt investments but have a provision that allows the principal plus accrued interest to convert into an equity investment at a later date. This allows the original investment to get done more quickly with lower legal fees for the company at the time, but ultimately gives the investors the economic exposure of an equity investment.

Typical Terms and Provisions of Convertible Notes

Interest : While the convertible note is in place, the invested funds earn a rate of interest like any other debt investment. The interest is not typically paid in cash, but accrued, which means the value owed to the investor builds up over time.

Maturity Date : Convertible notes carry a maturity date, at which the notes are due and payable to the investors if they have not already converted to equity. Some convertible notes have an automatic conversion at maturity.

Conversion Provisions : The primary purpose of a convertible note is that it will convert into equity at some point in the future. The most common method of conversion occurs when a subsequent equity investment exceeds a certain threshold. This is called a qualified financing. At this time, the original principal plus any accrued interest converts into shares of whatever new equity was just sold. In addition to getting the benefit of the accrued interest, which buys the convertible note holders more shares than they would have if they had waited and invested the same amount of money in the equity round of financing, they often get several additional perks in exchange for investing earlier. In the event that a qualified financing does not occur before the maturity date, some convertible notes also include a provision in which the notes automatically convert to equity, at a set valuation, on the maturity date.

Conversion Discount : When the convertible notes convert to equity in the event of a qualified financing, not only do the note holders get credit for both their original principal plus accrued interest to determine how many shares they receive, they also generally get a discount to the price per share of the new equity. For example, if the discount is 20% and the new equity in the qualified financing is sold at €2,00 per share, the convertible note’s principal plus accrued interest converts at a share price of €1,60 per share.

Valuation Cap : In addition to the conversion discount, convertible notes also typically have a valuation cap, which is a hard cap on the conversion price for noteholders regardless of the price per share on the next round of equity financing. Typically, any automatic conversions that occur at the maturity date (if no qualified financing has occurred) are at some price per share that is lower than the valuation cap.

Equity vs. Debt vs. Convertible Notes

Pros and Cons of Convertible Notes as a Funding Mechanism

Now that we have discussed the typical terms and structure of a convertible note, we will now take a look at some of the reasons why companies use them as a way of raising investment funds, and some of the drawbacks as well.

PROS

- Convertible note financings are simpler to document from a legal perspective. This means that they are generally less expensive from a legal perspective and that the rounds can be closed more quickly. The reasons for this are pretty simple, being that the company and the investors are putting off some of the trickier details to a later date. In most equity financings, numerous corporate documents need to be updated to close the round such as certificates of incorporation, operating agreements, shareholder agreements, voting agreements, and various other items. All of this adds to the time and expense of completing a round of equity funding.

- Raising a convertible note as opposed to equity allows the company to delay placing a value on itself. This is particularly attractive to seed-stage companies that have not had time to show much traction in terms of their product and/or revenue. In exchange for giving investors a discount on the price that is set later, the company is able to push that decision to a later date. Because of this, convertible notes are often used as the first outside funding invested in many companies, and a large number of institutional seed investors such as 500 Startups exclusively use convertible notes in their accelerator investments.

- For a variety of reasons, many companies need to raise some amount of funding between larger rounds of equity, and the features of a convertible note make it an ideal vehicle to complete those types of transactions. For example, one company that I have worked with had a transformational software deal with a large enterprise customer that was set to close. The company would need to ramp up its staff in order to service the new customer and was planning to raise a new round of equity once the deal was signed; however, they could not disclose the specifics of the deal until that time. In order to get a jump-start on the work once the deal closed, the company wanted to raise a smaller amount of funds via a convertible note as it would allow the funding to close more quickly. It would also allow the company to delay the valuation decision for the equity round, as that would likely be more favorable once they were able to disclose the full details of the new contract.

CONS

- While there are many reasons why companies and/or investors choose to utilize convertible notes, both sides of the deal really need to think through the potential future implications of using this method of financing. The biggest issue that I have seen with seed stage companies is the question of what happens if the company cannot, or chooses not, to raise subsequent equity financing. While many convertible notes do include provisions for an automatic conversion on maturity, many do not. Given that we are mostly discussing very early stage companies, most of these companies are burning cash, and will not have the funds to repay the note at maturity if it does not convert. The best way to avoid this situation is for both the company and investors to have a clear plan for both success and failure. In most cases, if a company cannot raise additional funding past an initial convertible note seed investment, it is because the company does not have traction and will either end up going out of business or being acquired for a nominal amount. One interesting example from my work involves a company that received a seed investment in the form of a convertible note from a startup accelerator, and was not able to raise additional equity funding, but was able to gain enough traction to continue operations and get to cash flow breakeven. The company did not have nearly enough cash to repay the note, but it was not going out of business either. However, if the investor foreclosed on the company, it would have essentially put the company out of business and guaranteed that their investment would be worth nothing. This left both the company and the investor in an awkward position that took several years to get resolved.

- The awkward situation of the company described in the preceding anecdote can be avoided by negotiating the terms of an automatic conversion at the maturity of the note. However, if you go too far down the road of defining what that next round looks like in regard to all of the terms and provisions that would be included in a typical equity round you actually lose some of the benefits of using a convertible note in the first place. One example related to a company that I have worked with involving a promising software startup that was graduating from an accelerator program. It had a basic product, some name brand clients had already signed contracts, and the company had attracted potential investors. They chose to fund the round with a convertible note but given that the note may have been enough funding to take the company past the maturity date, they wanted to know what their investment would be like if that happened. As it turned out, this led down the road to negotiating exactly what the specific terms of that equity round would look like, and the company ended up spending as much on legal fees as if they had just done the equity round to begin with.

- The majority of convertible notes issued in seed funding scenarios at this point in time include a valuation cap and an automatic conversion price. While you are technically delaying putting a price on the company, oftentimes the cap and conversion price effectively acts to anchor the price negotiations of the next round. Even if investors are willing to pay for a big uptick in valuation from the note valuation cap, you can end up with some very strange situations. For example, if the subsequent round of equity is preferred stock with a liquidation preference equal to the price per share of that round, convertible note holders can end up with a liquidation preference of several times their investment if there is a large uptick in valuation. In situations like this, the new investors may try to force the note holders to adversely amend their terms in order to close the deal.

EXAMPLE: A startup company with 1.000.000 shares of common stock closes a seed funding round of €1.000.000 in the form of a convertible note, with a valuation cap of €5.000.000 pre-money valuation on the next round of financing. For simplicity, assume the note carries a 0% interest rate. The company makes a lot of progress and has a venture capital firm willing to do a €4.000.000 Series A financing at a pre-money valuation of €20.000.000, with a liquidation preference of 1X. The €4.000.000 series A investment will buy 200.000 shares of preferred stock at €20/each, with each share carrying a liquidation preference of €20, plus any accrued dividends. Because of the valuation cap, the €1.000.000 convertible note will convert to the same type of equity at the rate of €5/share, but those shares will have a liquidation preference of €20/each plus dividends which means they would effectively have a 4x liquidation preference! It is highly unlikely the series A investors would allow this to happen and would likely require the convertible note holders to renegotiate.

***Source: The information from Executive Summary till this point is from an article of Jeffrey Briggs, Finance Expert at Toptal.com***

Understanding the basics

Is a convertible note debt or equity?

Convertible notes are originally structured as debt investments but have a provision that allows the principal plus accrued interest to convert into an equity investment at a later date. This means they are essentially a hybrid of debt and equity.

What is a cap in a convertible note?

A valuation cap is a hard cap on the conversion price for note holders regardless of the price per share on the next round of equity financing. Any automatic conversions that occur at the maturity date (if no qualified financing have occurred) are at some price per share that is lower than the cap.

How does a Convertible Note work?

Convertible notes are debt instruments that include terms like a maturity date, an interest rate, etc., but that will convert into equity if a future equity round is raised. The conversion typically occurs at a discount to the price per share of the future round.

MAIN KEY POINTS:

- A convertible note is a financial instrument that contains a written promise from one party (the publisher or creator of the note) to pay another party (the beneficiary of the note) a specified amount, either upon request or at a specified future date;

- A convertible note usually contains all of the terms and conditions related to the debt, such as principal, interest rate, maturity date, date and place of issue and the signature of the issuer;

- In terms of their legal enforceability, convertible notes lie somewhere between the informality of an IOU and the rigidity of a loan contract.

In this we are the issuer of the convertible note, in series, depending on the program the participant opts for. The participant acts as a lender who receives the convertible note with the said consideration. The convertible note has a convertible clause, whereby the principal is converted into shares within the projects or the parent company; P.T. Emas Cemerlang Bersama, the initiator of both projects.

This gives the participant the opportunity to profit from the growth of both projects and thus realize a financial gain at the desired moment after the conversion.

Startup Financing

We all know the success stories of startups and their almost improbable growth potential. But only a few of us can take advantage of this. Million dollar amounts are often mentioned in startup press releases as if it were some pocket money. When discussing the valuation of a startup, the million dollar amounts are the holy grail, they are always nice round numbers and a million or 10 more or less is no longer the distinguishing factor. We are probably too much of an entrepreneur to be impressed by that. We choose not to limit who is eligible to participate, we want the public to benefit from the growth potential of the projects. Participation in the Convertible Note and the relevant projects starts at an amount of €50,00, to be increased by the same amount each time. We manage the issuance of the Convertible Note ourselves. We do not wish to attract an unnecessary amount of funds, only to fill the company’s bank account. When we involve a financial institution in the issuance of the Convertible Note, they will make every effort to increase the principal amount, or they will charge a higher percentage of brokerage fees. We do not wish to participate in this. This would mean the wrong use of funds. Every agreement we enter with an investor/capital provider is a moment when we take on a certain responsibility. The capital provider expects us to handle his money well and expects a certain compensation in the form of a return on capital. That is why we only accept new funds that we can deploy in the foreseeable future. De Convertible Note zal worden uitgegeven in een serie van 2 tranches, met een verlengd maximum van 3 extra tranches, waarbij elke tranche een waarde van €500.000,00 vertegenwoordigt. The first two tranches follow each other immediately, from the third tranche we will first consult with the existing Note holders before releasing any new tranche.

At this stage of development of both projects, we need to keep an eye on the budget, set clear goals for what we need to achieve within the limits of the budgets. For both projects we must ensure progress within the budget of €1.000.000,00. The goal we have set ourselves for the collaborative robot is to realize a working prototype. The social program backed by a blockchain platform with crypto-token requires the social program to be fully operational and the blockchain platform to exist in beta. This should be feasible for the social program, but it will be a very big challenge for the collaborative robot to achieve these goals within the set budgets, however we also have internal budgets at our disposal, such as the sales revenues from our web shops.

This funding round is just the beginning for both projects. In the next development phase, the projects will be separated. While the collaborative robot will enter the next stage of development with a focus on the software side of development, the social program will be fully operational, and the focus will be on the next stage of development for the blockchain platform. It is expected that a fully independent legal structure will be realized for each project in the next development phase. A lot of work is currently being done to give the social program the right legal structure.

The reader may wonder why we are doing this round of funding under the banner of P.T. Emas Cemerlang Bersama and not directly in a separate entity? This is done solely to provide security to participants. If we let the participant participate in a new legal structure, the participant is investing in an empty shell that offers no security whatsoever in the event of negative circumstances. This is unacceptable to us as initiators. We are the initiators of both projects and will have to show a certain degree of responsibility. P.T. Emas Cemerlang Bersama guarantees the nominal amounts invested by the participants and the interest prepayments to be made. In each case, a reservation is made for the prepayment of interest at the end of each calendar quarter. These interest prepayments are not deducted from the principal. The company takes care of the interest prepayment directly from its own cash flow. This article discusses all the points of the agreement, but it is wise to highlight the principal at this point. The entrepreneur guarantees the principal sum that the participants will invest under this Convertible Note until the moment of conversion into shares.

The characteristics of participating in the Convertible Note series

This Note issue contains a series of Convertible Notes with a total value of €1.000.000,00. Two tranches of €500.000,00 each, with an extension of 1 to 3 tranches under the same terms and conditions. The funds will be used exclusively for the development of the projects. The participant is given the opportunity to spread the risk over two different projects within one investment. Two different industries, two different user audiences, so there’s real diversification. While we will use the funds for both projects at the same time, each project has its own unique trajectory. The first project, the collaborative robot, has a longer development path because it is a multi-complex problem (hardware and software problem) that we want to solve. Where in the second project we can proceed with the rollout in beta version of the Blockchain platform and Crypto Token after a relatively short time. The intended period that we want to be fully operational with the Blockchain platform is the last quarter of 2022.

The maturity date of the Convertible Note is 6 years (72 months). This duration period was chosen because we want to create sufficient value for each project, so that we can realize a successful share conversion to everyone’s satisfaction. The duration period should not be confused with the conversion event, which are two separate events in time. The maturity of the Note is a built-in guarantee that if the conversion does not occur for any reason, the Note will not have a perpetual maturity. As compensation for this period, P.T. Emas Cemerlang Bersama guarantees an interest of 6% per annum. Each participant has the choice to have the interest paid annually or quarterly in advance, or to use the option to build up the interest with the investment and have this total amount converted into shares.

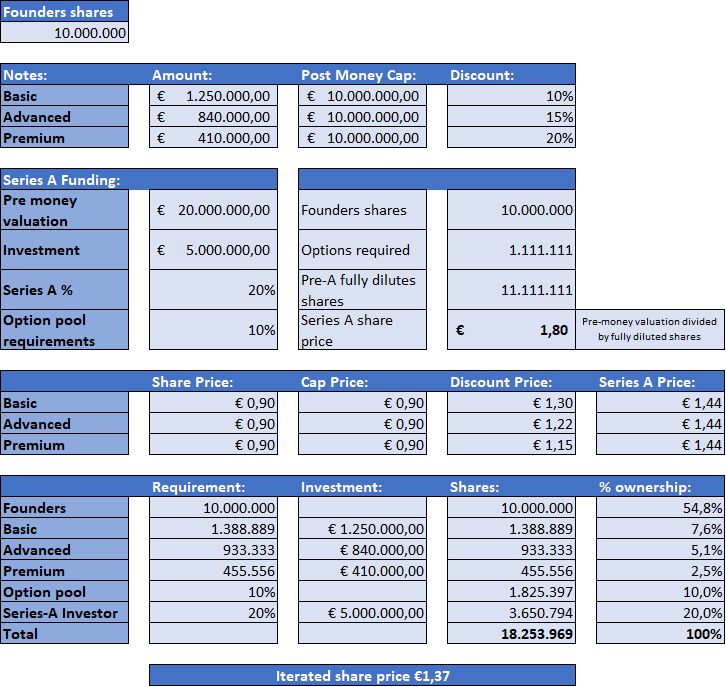

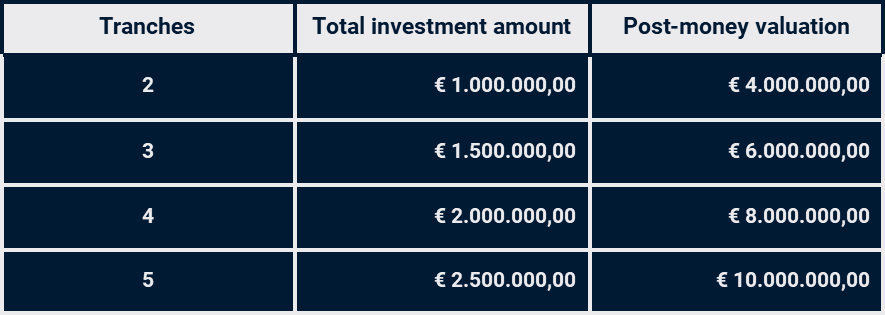

The conversion is activated as soon as a Series-A financing occurs. This is a new financing round in which the new investor wants to acquire preference shares in the company concerned with immediate effect. This is usually a second or third round of investment, where the product is available that reflects a certain value for future expansion. This will be a significantly larger investment than what we are currently rolling out. It is important that a valuation, reflecting a percentage of the company’s performance, is given to the Convertible Note that will be converted into shares in the future. The valuation under this Convertible Note is set at €4.000.000,00 of enterprise value. If the entire Series of Convertible Notes (5 tranches with a value of €500.000,00 each) will be issued to participants, the current and future business operations will have an imputed value of €10.000.000,00 (post-money valuation Cap), including the investment amount of €2.500.000,00 (if all 5 tranches are issued).

This is a fair valuation as the current operating value of P.T. Emas Cemerlang Bersama is estimated at a minimum of €7.500.000,00. We are not sure about the valuation of the side activities of P.T. Emas Cemerlang Bersama (companies under management) as these are uncertain times. This is too uncertain a factor, which is why we do not include them in our valuation at the moment, but they are expected to represent a book value at the end of the 2021-22 financial year. Not all secondary activities can be converted into liquid assets in the short term, which is another reason not to include them in the valuation of the company. Until the conversion takes place, P.T. Emas Cemerlang Bersama guarantee the full investment amount and interest payment.

In addition to this Convertible Note, which is not yet accounted for at the time of writing, P.T. Emas Cemerlang Bersama has no external debts other than with its own shareholders/founders. We have not incurred any operating losses in the past 4 years, 2017-2020. The shareholders declare that they are not entitled to these monies until the conversion has taken place and will not take on any other shareholders until conversion, except in extreme emergencies. Nor have any shares been pledged to third parties. A minimum of 25% of the shares will be reserved for participants in the Convertible Note.

Tranches, Series and Programs

The Convertible Note contains 2 tranches of €500.000,00 each. We will begin raising funds for the first tranche as soon as this writing is published. After reporting development progress, we will release the next tranche for participation. Consultation with Noteholders of previous tranches will decide whether to raise funds for one or more tranches at once. We don’t want to raise funds that we won’t use in a reasonable amount of time. When all Notes in a tranche have been issued to participants, subsequent subscriptions will be accepted as reservations for the issuance of new tranche(s), the Notes will be allocated in order of subscription received.

The Convertible Note will be issued in a series of Notes from €50,00 up to €2.000,00 per Note, with a maximum of 10.418 Notes for an aggregate nominal value of €1.000.000,00. Each tranche contains 5.209 Notes – 5.000 Notes under the Basic program with a participation value of €50,00 each, 168 Notes under the Advanced program with a participation value of €1.000,00 each and 41 Notes under the Premium Program with a participation value €2.000.00 each. A Note is not divisible, each Note must be registered by a person or legal entity, multiple owners per Note at the same time is not possible. A Note is transferable to a third party, but P.T. Emas Cemerlang Bersama must be notified in advance to register the new Noteholder before the third party can derive any rights from it.

Participants may choose from 3 different programs; Basic, Advanced and Premium. The different programs do not affect the number of shares per Note that will be allocated upon conversion. Each Note within a program will be allocated a proportional number of shares with the conversion, but the number of shares the participant will receive varies by participation amount, program, and any additional conditions. For the conditions of the various programs, we refer to the explanation on our website: www.emcebe.com/participation/.

There are differences in the Nominal value of a Note for each program, participation within the basic program starts at €50,00, the nominal value of a single Note. Participation in the Advanced program starts at €1.000,00 for a single Note and within the Premium program the Nominal Value of a single Note is €2.000,00. We want to present the projects to a large audience and that is why we have decided to limit the participation per participant to the principal sum of €2.000,00. This means that if a participant only wants to get Notes in the Basic Program, the participant will be allocated a maximum of 40 Notes. For the Advanced program a participant receives a maximum of 2 Notes and for the Premium program 1 Note per participant. Or a combination of 20 Notes within the Basic program and 1 Note within the Advanced program. This limitation only applies to the first tranche of the Convertible Note. Participants can indicate which program they want to participate in; however, it is in order of registration whether participation in the relevant program is possible. It is not possible to deviate from the number of Notes for the Premium program; this will always have a maximum of 41 Notes for each tranche. It is up to each participant to decide which program to participate in, if available.

The following differences between the programs can be found in the conversion discount. This is the discount for which the participant can receive the shares when the conversion takes place. This discount is respectively 10%, 15% and 20% for the Basic, Advanced and Premium program. Later in this document, it will become clear why this can be of great importance to clearly consider which program the participant wants to participate in. Then there is another noticeable difference in participation within the Premium program, compared to the other 2 programs. Participation in the Premium program is classified as a senior debt, while participation in the Basic and Advanced program is classified as a junior debt. You can read more about this in the further explanation of the agreement later in this document.

One last difference to notice. If a participant purchases a product via our online shop, there is a discount on the purchase price of the goods of 5% for participants in the Advanced program and for participants in the Premium program of 7.5%. This discount only applies to the purchase price of the goods, shipping costs and any import duties are not included in this discount, which is entirely at the buyer’s expense. The discount also does not apply to items offered during any sale period. Participants in the Basic Program can always buy products from our online shop but will not receive a standard discount. With every purchase of items from our online shop you support the innovation projects, as all profits that we realize from the sale of these items become fully available for the projects.

Besides any financial gain, what are the benefits of participating?

By participating, the participant has the unique opportunity to experience what investing in a startup entails. We all know the success stories of big Tech startups, such as Facebook, Google, Apple, Microsoft and of course the Dutch Adyen and less associated with Tech but still in the startup category, Amazon, Tesla, Uber. Each one of them has created millionaires and billionaires. Who has never wondered: “If only I had been able to buy shares in those companies early in the start-up phase”? It’s always the same group of people who make money from this, either you have to work for these companies so you can qualify for employee stock options or be an angel investor. They depend on the public to use their products, but it is not the public that gets involved in the startup investment and thus reaps the financial benefits.

But let’s face it, startup financing is not for those with a “weak stomach”. There is usually no frame of reference, which means that the financial valuation of the start-up at an early stage is often “a gamble”. If you invest in a startup, you have to dare and be able to see through a lot of fog. There is nothing more changeable than the road to success that many startups have to take. Success is certainly not guaranteed, but when a startup is successful, it is a multiplying success. Stories of multiplying your investment dozens of times is certainly no exception. It is considered normal that if only 6X or 7X is achieved on the investment, it is only a meager success. If you want to immediately get rid of your investment in the event of a first setback, do not invest in a startup. NEVER invest with money you can’t afford to lose. If it is said that there are no guarantees in investing, then that counts for 1.000% towards investing in a startup. As “easy” as it may seem to get back a multiple of your investment amount, it’s even easier to let it end in disappointment.

Investing in a startup is not for greedy characters as you will always end up disappointed. If the return on investment is not in line with your expectations, the sentiment will be negative, even though the result may be positive. When returns exceed expectations, you’re left wondering why you haven’t invested more. Investors make more wrong decisions out of greed than out of prudence. The same goes for stingy characters, if you don’t want anyone to share in the opportunity, chances are you’ll block success with that, because there really aren’t that many people who can financially support a startup all on their own. Those who cannot share have less chance on multiplying.

Never invest in a startup if you have set a goal for the return in advance and take that as the reason for making the investment. Start-up financing is not a supplement to your pension, nor is it a supplement to the study fund for your children. With a startup, the end date is never clearly known in advance, postponement is almost 100% guaranteed, so don’t count on an outcome when it suits you, you will be disappointed. That you then spend the return on your investment in the startup on a goal, your pension accrual, the study fund, that’s what you do it for, you have taken the risk, you are rewarded for it, so enjoy the result. But it can never be the reason why you invest.

Then why invest, because of the experience that the participant gains with this. With no other investment in a company, you get the chance to go through so many different phases in a relatively short time, whether in financing, growth or product development, everything happens much faster than within a traditional company. It is not up to every entrepreneur to lead an innovation start-up, on the other hand almost no founder of an innovation start-up feels suitable to guide the company through the next phase. The only ones who haven’t switched seats at a successful startup is Amazon’s Jeff Bezos, maybe Facebook’s Mark Zuckerberg, but that’s about it. Even the highly acclaimed Steve Jobs at one point felt inadequate to lead the company’s next phase, partly under pressure from shareholders.

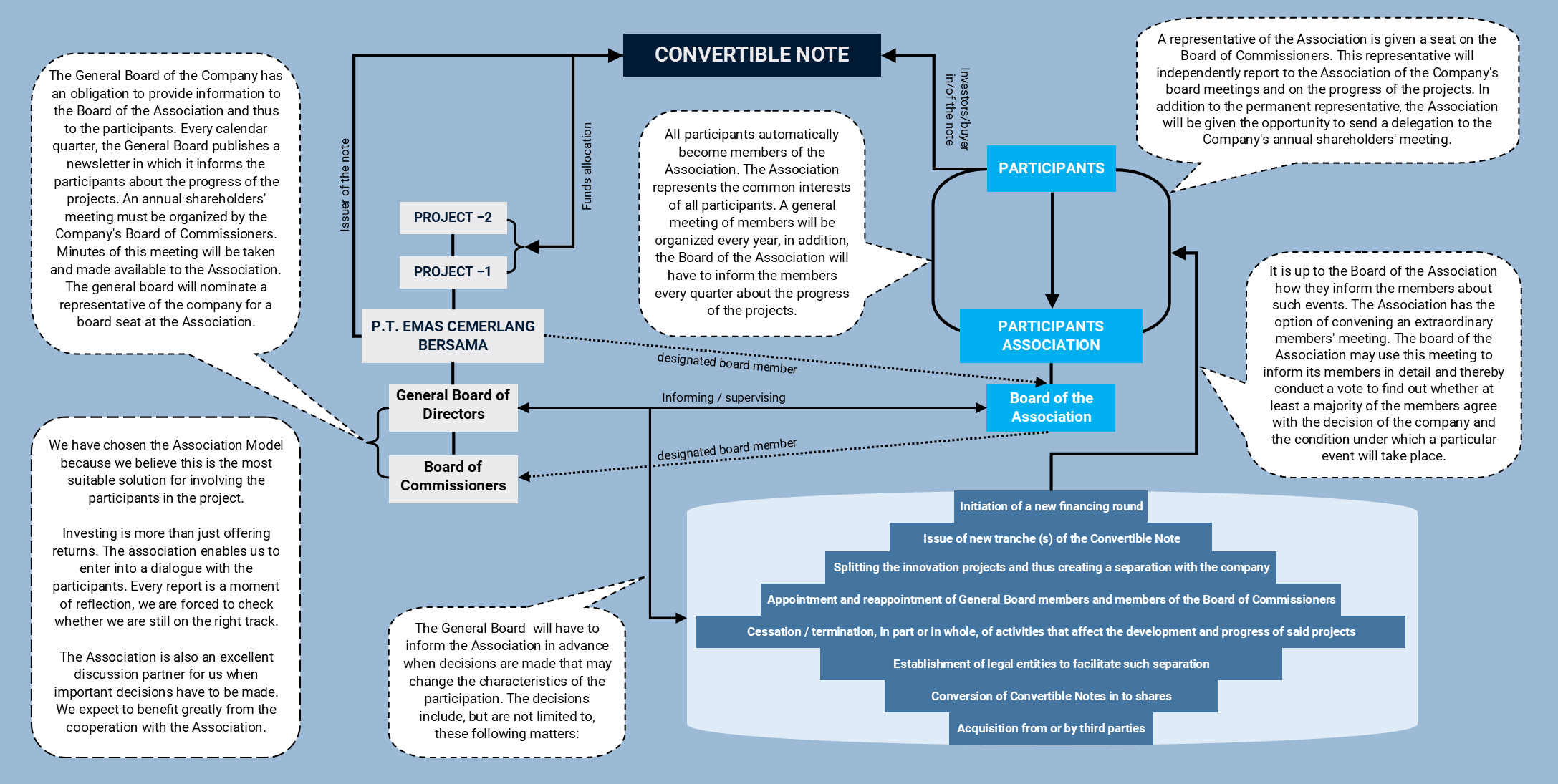

If the participant is interested in experiencing all of this, regardless of the final outcome, the investment is sure to be a resounding success. Now we can’t control what other startups are doing, but we will involve the participants every step of the way. We even want to include a representative of the participants in the supervisory board. Monthly we report to the participants association and every quarter we report and publish on the progress of the innovation and operational activities of the company. Although they are not consumer products that we develop, ultimately the public will certainly benefit from the products. Where necessary, we will involve the supervisory board in strategic decisions, where the delegate of the participants has a seat. There is also an annual general shareholders’ meeting in which the supervisory board has an important vote in the initial stage and later the shareholders themselves.

From a minimum participation amount of € 50,00, each participant receives all information from the report, or at least the link to the information published on our website. Participants can contact us directly with questions and/or comments. In addition, we will oblige the participants’ association to maintain contact with all participants. To our knowledge, this is a unique approach, as it is highly unusual for early investors to sit on the supervisory board. We made the decision to do this anyway, because we think that the first participants are one of the most important investors. They drive the flywheel so that everything can be put into operation. After the conversion into shares, the association is dissolved, the participant immediately becomes co-owner of the project company with all available information. Perhaps the participants/shareholders can decide to continue the association, although this will no longer be facilitated by us, because we then have to treat all shareholders, old and new, equally.

The biggest advantage for the participants is that they have direct insight into the progress of the investment for a relatively low amount. A participant is not excluded because of the size of the investment amount. This cannot be said of traditional business investment. The participant does not have to make a 6-figure investment to be seen as full and to experience involvement in the progress. We have deliberately opted for public participation because we believe that everyone should be able to benefit from it and not just a select few that can reap the benefits themselves.

Because we make a direct investment possible, the participant does not pay any administration or management costs, our business model is not to manage the participant’s investment, but to enable innovation. Such costs are therefore not passed on to the participant. The same reason can be found why the participant makes the transaction directly to us and not through a payment processor. The costs involved; this can be up to 11% if we include the currency transaction costs. We can really put this money to much better use. We may miss out on a number of participants, but we choose to be efficient with the resources made available to us, rather than ease of payment. It is a one-time transaction and not a monthly payment.

Association EmCeBe

The Association represents the common interests of all participants. All participants automatically become members of the Association, participants themselves determine their involvement in the investment and the Association. Once all Notes within the first tranche have been issued to participants, the participants’ association will become operational. Initially we will appoint an independent board, but a delegation of the participants will have to fill most of the board seats. After the full board of the Association has been installed, the Association will have to nominate a representative who holds a position on the Board of Commissioners of P.T. Emas Cemerlang Bersama.

The Association keeps a membership administration and a participation register, this participation register is updated every quarter following the notarial confirmation of participation/investment. The “original” register of participants is managed by the company, after which the civil-law notary will confirm the changes in this register and report it to the Association every quarter. Each year, a delegation from the Association must attend the shareholders’ meeting of the projects and the initiator of the innovation projects. After this meeting has taken place and the annual reports have been sent to all members, a meeting will be organized. This is the general members’ meeting; this is a mandatory annual meeting that the Board of the Association must organize.

In addition, the Association has the option of convening an extraordinary meeting of members. This is a tool that can be used to organize a vote on certain important topics. For example, if we, P.T. Emas Cemerlang Bersama, decide to split off one or both projects, the Association can convene an extraordinary meeting of members. The board of the Association may use this meeting to inform its members in detail and thereby conduct a vote to find out whether at least a majority of the members agree with the decision of the company and the condition under which a particular event will take place.

After such a vote, the Board of the Association will have to formulate an advice and submit this via its representative to the Board of Commissioners of the company. This advice of the Association should not be seen as a final decision, it is some advice to the General Board of the company. However, the General Board cannot simply ignore the advice of the Association. If the Board finds that they cannot follow up on the advice of the Association, they will have to formulate this and inform the Association about their decision. The General Board must explicitly consider that if it goes against the advice of the Association, it will have to deal with dissatisfied participants. If the decision of the General Board has far-reaching consequences for the participants and their interests, the Association may request an extraordinary shareholders’ meeting of the Company through its delegated commissioner. Such a request for an extraordinary shareholders’ meeting should be regarded as a last resort and should always be honored by the Board of Directors and its Board of Commissioners.

The General Board of P.T. Emas Cemerlang Bersama and its Board of Commissioners will have to inform the Association in advance when decisions are made that may change the characteristics of the participation. It is up to the Board of the Association whether to convene its members for a vote. The decisions about which the General Board of the Company must inform the Association prior to the relevant decision include, but are not limited to, the following matters:

- Issue of new tranche(s) of the Convertible Note;

- Initiation of a new financing round;

- Acquisition from or by third parties;

- Splitting the innovation projects and thus creating a separation with the company;

- Establishment of legal entities to facilitate such separation;

- Appointment and reappointment of General Board members and members of the Board of Commissioners;

- Cessation / termination, in part or in whole, of activities that affect the development and progress of said projects;

- Conversion of Convertible Notes in to shares.

The General Board of the Company, together with the Board of the Association, draws up a list of priorities in which the above matters are included and, where necessary, supplements it with other matters that the General Board must adhere to regarding the provision of information to the Association. However, the company reserves the right to designate certain matters as confidential and thereby impose the obligation on the Board of the Association to regard and treat the relevant information as such. This means that not all members/participants will be informed in advance, but this should be considered an exception and should therefore only be applied in extreme necessity. The rationale for the decision to pre-qualify certain information as confidential will have to be included in the information provided to Members when such matters are shared with Members afterwards.

Finally, we would like to emphasize that the company reserves the right to suspend or dismiss one or several board members in the event of improper management. This is especially true if mismanagement by a certain board member or several board members could harm the participants and/or the projects and the company. When such acts come to the attention of the General Board of the Company or the Board of Commissioners, it will first inform the Board of the Association. If the Board of the Association does not take adequate measures against the member or members concerned, the General Board of the Company may take measures whereby the member or members concerned may be suspended or expelled. In the event of a suspension, this is of a temporary nature, for example if further investigation into the facts will have to take place. The member or members concerned will be given the opportunity to defend themselves against the allegations, the decision will always be communicated in writing to all board members. In the event of a dismissal, this is of a permanent nature and cannot be appealed against. The relevant board member also loses his membership of the Association. It is up to the Company to further settle this with the person or persons involved. Taking such measures is only possible in extreme necessity and when direct or indirect damage to participants, projects and/or company can be demonstrated. It is up to the members to nominate a new Board member.

A closer look at the agreement

Here we explain the agreement in more detail per article and describe what we think needs explanation. However, this does not mean that the reader may not have further questions. If a certain article or topic is completely or partially unclear, please let us know immediately. All our contact details are listed at the beginning of this document. You can also reach us through our website: https://www.emcebe.com or via the chat function of the platform on which you are reading this document.

Article 1. Interpretation

1.1 Definitions: This one speaks for itself, it should be clear what all the terminology means if one reads the description, if not clear, let us know.

1.2 Interpretation: The same applies as under 1.1.

Article 2. Conditions

2.1 Conditions:

A. The Note is issued with the following condition: A statement will be prepared and made available by the directors and other shareholders of the company (if necessary) that they are aware of and agree to the issue of the Note and its terms.

To the extent necessary, the existing shareholders voluntarily waive any (existing) pre-emptive rights with respect to the execution of the Note and any issue of Conversion Shares;

B. that the company enters into agreements with other investors within these series under the same terms and conditions, except for the amount of the investment. The investment amount of the Notes in this series are from €50,00 for Notes in the Basic Program up to €2.000,00 for Notes in the Premium Program, within this tranche 5.209 Notes will be issued for a total amount of €500.000,00. Within the entire series there are 2 tranches of €500.000,00 each, which equates to 10.418 Notes with a total investment amount of €1.000.000,00.

2.2 Non-fulfilment: If the conditions, as stated in 2.1 are not realized within a period of 90 days, the agreement will be dissolved. When the Note is canceled within this clause 2.2. neither party has any obligation to each other than termination of the agreement. In other words, if the company does not comply with the condition mentioned in 2.1, the agreement will be dissolved, and the investment amount will be returned.

Article 3. Investment amount and terms of the note

This entire article may be clear, the investment amount must be transferred in its entirety in 1 transaction to a bank account that the company makes available for this on the date as agreed. The company may not use the funds for anything other than the projects or otherwise agreed with a majority of participants in these Note series. Clause 3.4 equals 2.1B.

Article 4. Conversion

This article deserves special attention. It will be a topic of discussion as long as the investment will last. Even after the conversion has taken place, it will continue to be discussed. This is the moment when it becomes clear what the return on investment will include. The conversion will take place when a qualifying equity financing takes place whereby new shares are issued to the investors of this financing. On the day these new shares are issued, the conversion into shares will also take place for the participants in the convertible note. Since this is a new round of capitalization for the company, it will receive a higher valuation than at the time of the issue of the convertible note. This means that the participants of the convertible note will get a better conversion value.

Below is a calculation example to provide clarity, no rights can be derived from the numbers used in this calculation example and the result.

At the time of full issuance of the convertible bond, the whole (current estimated enterprise value + the required investment sum) will receive a financial valuation of €10.000.000,00 (Post Money Valuation). This is the valuation if the 2 tranches in the current Note are purchased by participants plus 3 tranches with a possible extension of the issuance of the Note (Total investment amount €2.500.000,00). Each full tranche issued will have a valuation of 5% of the total enterprise value as stated above. We, the company, and the participants, will benefit more from a lower (moderate) valuation in the long term at this stage, the valuation will be as follows:

Then there are a number of situations conceivable where the investment comes to a halt. The agreement deals with these situations as completely as possible, if a situation is not included, then the approach is in any case clear. In all cases it will be clear that the participant will not be able to make an individual decision, it should be a decision by majority. The association will not be bypassed in the decision process, they will have to conduct a vote to know what de majority decision in a particular situation will be. In every situation, the company is obliged to inform the association in advance and ask for a decision.

In the event of a liquidity event, see the definition list (Article 1 of the Agreement), the investor / majority of investors will have to decide whether to agree and offer the Note for conversion. Should an individual participant, or majority, decide not to submit the Note for conversion, the company is obliged to pay out the investment amount, plus an additional amount equal to the investment amount plus unpaid interest payments, within 20 business days of a liquidity event, to this participant(s).

Then there is the conversion expiration date. This is in the exceptional case that we do not attract any investments other than this Note investment. Then the Note expires in 6 years, or sooner if we decide this jointly with all participants. The company will then have to issue new shares within the company and allocate them for the participants. Together with the association, we will arrive at a conversion rate where all parties, including ourselves, can be satisfied with.

All other points within this article discuss the implementation and provisions under which a conversion must take place. We think these points speak for themselves, if anything is not clear, we advise you to contact us immediately and we will (try to) answer all questions.

Article 5. Interest

The interest is an annual simplified interest, not interest on interest (compound interest) payment, but 6% interest on the investment amount on an annual basis. This interest is paid as soon as the investment amount is converted into shares, the interest can be added to this. In the event that interest is paid to the participant annually or if the participant claims his investment amount, the following article 6 discusses this in more detail.

Taxes: This is up to each individual investor to determine whether or not tax should be paid on any interest. We do not make any statements about this, as we do not know what everyone’s personal financial situation will be. We will have to register when we make a physical interest payment to one or more participants.

Article 6. Repayment and Prepayment

The company undertakes to pay the investment amount, with any outstanding interest, to the participant within 5 working days when he claims it through a written claim. However, the participant confirms with the signing of the agreement that such a requirement will not be issued before the expiry date.

The investment amount is not eligible for an upfront payment, before the Note’s expiration date or a liquidity event. The participant may require a pre-payment of the interest, however after the annual interest has been allocated.

Article 7. Company’s Undertakings

The company must not act contrary to this agreement. No changes may be made within the company that could be detrimental to the participants. If a situation arises that could endanger the survival of the company, the company will have to inform participants at an early stage and clearly explain the steps to protect participants from any injustice. Should the company fail to do so, the board can be held responsible and liable with all the consequences that entails such.

Article 8. Insolvency Events

This article sets out under what circumstances an insolvency event can take place.

This gives the participant the right to make the investment claimable.

Article 9. Warranties

This article is self-explanatory and should be clear to all participants. The company guarantees the participant that the company is a legal entity that is existing since 2015, not just established for this purpose only. Any subsequent company will be incorporated by law and must obtain all permits and licenses in order to operate properly.

To the extent necessary, the company holds the intellectual property of the developments or, where necessary, we will register the intellectual property in order to collect and retain all rights to protect the project and the rights of the company and participants.

With the innovation we do not violate any intellectual property rights of third parties and thereby also declare that we are not involved in any legal proceedings from third parties that claim the right to any development that we carry out.

Article 10. Additional Investor Rights

Points 1 and 2 speak for themselves, we fulfill these rights by considering the association as such and by sharing all reports directly with the association. In addition, we will share financial information with all participants every quarter.

Point 3 of this article relates directly to the participants in the premium program. At least for the nominal investment amount, they may purchase additional shares for the same conditions as the new investor enabling the conversion.

All participants are eligible if they are willing to make the next investment for a minimum of € 10,000.00. We may not make an offer to any investor / participant if local law in the relevant country of origin of the investor / participant does not permit this.

Article 11. General

All points under this article should be clear.

Article 12. Governing Law

We are an Indonesian company, so it goes without saying that the Indonesian legislation on this agreement applies in the first place. However, where possible, we will make this agreement applicable to international law if it will not harm the interests of the company or its participants.

Article 13. Dispute Resolution

This article may be clear.

In the realization of the agreement, we took the interests of both parties into account as much as possible. We have come to the conclusion that this agreement fully guarantees the investment and we have done everything to provide both parties with sufficient security. Risks will be limited to a minimum, but certainty can never be guaranteed when it comes to return or the outcome of the investment.

Partly through the establishment of the participants association, we provide a wide opportunity for the participant to participate in the policy making of the company and innovations. We commit ourselves to keep informing the participant about every step in the process that we want or have to make. Everything will have to be done to realize both projects.

Our expectations for the projects

Objectively, it is difficult to sketch a scenario at this stage of development. It can still go in all directions, both with the development of each project and with the trajectory to be followed. But if we didn’t support one of the projects, we would never realize them, or enter into agreements with investors/participants for an investment.

We are very positive about both projects and see a very bright future for each project. For both projects, this investment, which we now want to involve the public in, will not be the last investment round. This is one of the reasons why we find this form of financing extremely suitable, the Convertible Note. This allows us to only raise funds that we need at each stage of development. That is why we opt for the tranche model. It forces us to be fully accountable every time about what we have achieved with the funds and what we are going to spend the new funds on.

Each project will have its own trajectory. The Community Welfare Program project has 2 different facets, on the one hand we have the social program, on the other hand we have the development of the Blockchain platform and crypto token. While the Community Welfare Program is relatively easy to roll out, the start-up phase will require a lot more focus on the development of the Blockchain platform and all its applications. We are already working on a very small scale with our own resources to structurally help people in our society according to the philosophy of the Community Welfare Program. This can easily be rolled out on a larger scale, although we will add neighborhood community after neighborhood community, the difficulty will be more in the adoption of the Community Welfare Program by the members. Guidance and education will play a major role here.

As long as we roll out the program in a society that is equivalent to where we are going to start, essentially not much will change. Further expansion is then very easy and the speed with which it is rolled out depends on the financial resources we have available for the program to allocate to the members. Both projects can benefit if we can realize a rapid and successful expansion. The implementation of such a project in a society will receive a lot of attention from the media and civil society organizations, which will benefit both projects. In addition, the number of members will also influence a successful adoption of the blockchain platform.

The development of a blockchain platform and its applications is of a completely different caliber of innovation, development, and exploitation. The interests involved are so overwhelmingly determinative of all operational activities that it can be frightening. Every step in the development will have to be carefully considered, because a wrong decision in the beginning can have disastrous consequences for the further future of the platform. For that reason alone, we are not going to develop a blockchain protocol ourselves at this stage of the project. We will join an existing concept and develop it further into a blockchain platform for our own objectives. Which blockchain protocol we will choose is not yet 100% known. We narrowed down the choice of dozens of blockchain networks to a shortlist of three candidates:

- Algorand

- Avalanche

- Cardano

This is arranged alphabetically and says nothing about the final choice of the candidate blockchain protocol. If the reader is curious about our motivation for narrowing the shortlist to these three candidates and what it entailed, please refer to the project documentation published on our website[4].

The main question that will remain with the projects is of course; do we really need a blockchain network and crypto token to run the Community Welfare Program? Another question here will also be whether the investment is actually used to make a donation to a social community project? (Philanthropy in disguise) The first question, the answer is a resounding yes. The most important aspect of this answer is that we are going to manage the infrastructure independently with a token to capitalize on. In other words, we can apply value creation that cannot be exploited in any other way. A good example is you can build a highway, but without a revenue model it becomes an expense, while as soon as we charge costs for its use, you create a revenue model, which gives the value of the highway an intrinsic value. This is very important to create stability and trust for the Community Welfare Program.

Only a token could still be seen as a cheap form of grabbing quick money and profiting from the hype, but that’s not what we’re about at all. The Community Welfare Program will also not be a program where we give a certain amount to the members and they have to figure out for themselves what they are going to do with the money. You don’t solve the wealth gap problem by throwing money at it and thinking it will make your problems go away. We will have to structurally change the mindset of the members. Yes, we give the members a certain hope, but then our job is to guarantee stability by making sure that that hope can no longer be taken away. We’re going to provide the members with a certain amount of money that they couldn’t get their hands on in any other way than through luck, for example winning a lottery or maybe an inheritance from an unknown family member. What then is the sum of money which can give a certain hope? This is highly dependent on the community in which the program is deployed. We have concluded that it works best for us if we use a quantity related to its environment. That is why we arrived at twice the average annual income of the members, where you have to see members as families of a certain community, so the members are not individuals, but family compositions.

When that amount of money becomes available, you can attach an objective to it. Several programs have already shown that a money transfer works best if it has an objective attached to it. In general, the aim will be to spend the resources in such a way that the assets are expanded into a stable basis that can later be used as a financial safety net, for example as a retirement provision, a financial reserve in time of need, as a down payment for a house or as an education fund for the children. Although we would like to see other solutions created within the blockchain network for the latter, the study fund. Blockchain technology is going to make a very important contribution to provide the members with security, security in the sense that it can no longer be taken from them, assurance that everything they do within the program will also be theirs.

How can that security be guaranteed by blockchain? Read Satoshi Nakamoto’s white paper and you’ll understand what we’re talking about. Then dive into the white papers of the protocols we mentioned above: Algorand, Avalanche and Cardano and you will be completely convinced of what we are trying to explain. An X number of crypto tokens will be associated with each credit reserve allocated to the members. The members therefore get an identity and right to exist within the blockchain, every transaction they are going to perform will be registered, all of this can never be taken from them. A country or community can prohibit the use of crypto tokens as legal tender but can never ban blockchain protocols or even threaten the existence of crypto tokens. It cannot be expropriated once it has been granted. With every transaction that is registered, a member builds up history, which can be used again within the traditional financial industry. In other words, we are giving the opportunity to those members who mainly did not have access to traditional banking facilities to do so in the future. The motto used by many in the crypto world is making the unbanked within this society bankable again. That’s exactly what we’re going to do right away, action and not just some empty phrase.

We will have to explain what the rest of the world will gain from all this, because not the whole world will join the social program as member. We understand we need investors interested in adding the token to their portfolio. Then we will have to offer them something that will also benefit them. Or at least demonstrate that the platform is viable so that the token represents a certain value. We refer to the project documentation that covers this topic[5]. Then there will still be the question of what all of this will do for the investors in the Note? Once the blockchain platform and crypto token are available, Note holders will be able to exchange the Note for tokens at a discounted rate. We cannot yet elaborate on the value of the token that we envision, but we guarantee that investors in the Note will be more than satisfied with the expected value if they decide to exchange the Note for tokens. Does this mean that they will no longer be eligible for shares later? If participants choose to exchange the Note for tokens, they also waive the right to shares within the company. However, we will create an opportunity for all original Noteholders to participate in due course, in the same funding round in which the share conversion occurs, at the market conversion price that the Note will have.

Where the future of this project will lie is not entirely in our own hands, we depend on the adoption of the tokens, even if it is only a small part of the whole project. It is what makes any value tangible so that others can also have faith in the project and the Community Welfare Program. We will do everything we can to develop the project in such a way that everyone sees an interest in it and can start using the blockchain platform and the crypto token. Unfortunately, we cannot provide a timeline within which this should be fully completed, but the blockchain platform and crypto token should be publicly available for use by the end of 2022. We are now in the testing phase of the various protocols, and we will soon announce a final choice on which protocol we will develop. Keep following the blog on our website for more news about the developments.

Then the next innovative project, this one is of a completely different caliber. With a road map that cannot be compared. We are talking about both a hardware and software issue here. It will take much more time to present a working production model. But within the budgets of this investment round, our goal is to be able to present a prototype. This will be the focus of attention, it will be a very big challenge to achieve this with limited resources, but nothing is impossible. We have invested already our own capital in research. As a result, we know quite accurately which requirements the prototype will have to meet. But this is just the hardware side of the whole project. If we can present a working prototype that reflects our philosophy, we are confident that there will be more than enough candidates willing to join us for future funding. The amounts involved in the total development of the collaborative robot significantly exceed the total budget of the other project, where we are already talking about the exploitation phase in the other project.

We are confident that we will be able to develop a working prototype within a period of one and a half years, but the question is whether this will be a semi-autonomous working prototype. It is expected to have a remote control function with a human operator who will guide the collaborative robot through the operational procedures and closely monitor the execution. To achieve this goal, we will have to go through 2 phases. The first phase is the development of the prototype and the second phase is the storage and processing of current production data of the human movements. The how and why of the 2 phases will be described in more detail in a subsequent article.

We will do everything we can to realize both phases within budget. If we succeed, the way will be cleared to separate this project and develop it further in a purpose-built entity. This separation from the project will also be triggered by the conversion event and will be executed at the same time. We leave it to the participants to decide whether they want to continue with the investment or whether to treat it as a liquidity event and thereby terminate the participation. In all cases we will fully inform the participants and at that time express our expectations for the further future. The lead time for this will again be a maximum of 3 years, whereby we see the term as very long, because we try to achieve the realization of a prototype within a year and a half.

Epilogue

There will be 2 more documents in this series, both documents will each deal with one of the projects. We recommend the reader to follow our blog: www.emcebe.com/blog/. Here the reader can find out more about us and get further updates. If the reader has any questions and/or comments, we can be reached at: support@emcebe.com. Further contact information can be found at the beginning and the end of this document.

We are very positive about the prospects for both projects, two completely different markets, each with a different user base. The time pressure on both projects is not dictated by market dynamics, but pressure imposed by us, mainly because we want to continue to perform and not get stuck in further development. Bringing a project/product to the market means that it is the best and most honest test ground. The market will tell us exactly how the projects are doing. But because the market doesn’t impose that time pressure on us, we can take advantage of that by being allowed to perform, but not having to perform, in other words: it doesn’t have to be 100% perfect from day one. In this way we give ourselves the space to go back to “the drawing board” if we receive signals from the market that it is not yet good enough.

This gives us a margin of error where we are not charged for any mistakes in the beginning, we get the time to come up with a better product and satisfy our customers and investors. Performance allows us to appropriately reward the trust our investors place in us. We are convinced that we have built in sufficient certainty to achieve a positive result. The time, effort and financial resources that we have already invested in both projects support us in that belief.

We attach great importance to the establishment of the association of participants. We see the association as an additional consultative body, which we benefit from in various ways. This guarantees a closer involvement of the participants in the investment and development of the projects. Every report we send to the association is a test for us whether we are still on the right track. If we are regularly called to account for the work we do, we are automatically obliged to think carefully about the steps we take. In addition, we expect solid input from the participants if they discover shortcomings or have questions about the information, which in turn helps us to navigate further on the topics discussed.

We have deliberately kept the participation price as low as possible and will therefore arouse the interest of a larger audience. It requires more organization on our part, but with that we achieve the goal of making it a public participation and not just suitable for an elite group of investors who really don’t shy away from one investment more or less. We hope to give participants insight into what is involved in investing in a startup and go through all phases side by side with us.

Although we are very positive about the projects, we would like to point out to everyone that there are risks associated with any form of investment. We have succeeded in keeping the risks to an absolute minimum, but we cannot give any upfront guarantee about the end result of the investment. There are several factors that are beyond our control, including:

Currency risk

What is currency risk? Currency risk refers to the losses that an international financial transaction can incur as a result of currency movements. The value of an investment may fall as a result of changes in the relative value of the currencies involved. Investors may be exposed to currency risk when investing in different jurisdictions because exchange rates fluctuate.